This text has been translated by a machine and has not been reviewed by a human yet. Apologies for any errors or approximations – do not hesitate to send us a message if you spot some!

The very sharp price rises on the wholesale electricity market in 2021, after ten years of relative stability, raise fundamental questions about their underlying causes. It is therefore necessary to take a step back from the functioning of the electricity market and the mechanisms put in place around it.

In 1996, European directives required all member countries to set up an electricity market. 1 as with other public utilities (railways, postal services, telecoms). In all countries, electricity has been partially privatized. In France, EDF’s public monopoly has had to make way for competitors, notably with the stated aim of lowering the prices paid by consumers.

In the 20 years since its inception, the market has undergone constant transformation to overcome the many difficulties it has faced. But is the market “fixable” in a sector with very specific technical characteristics? Does it accelerate the energy transition or, on the contrary, hinder it?

To shed light on these issues, we present a description and analysis of the functioning of the electricity system and the electricity market, focusing on the French case. Our aim is not to advocate a return to the pre-competitive situation, but to understand how the liberalization of the electricity market has manifested itself and what its consequences are. This is necessary in a context where current market malfunctions will lead to new European negotiations under the leadership of the Commission.

The electricity system: characteristics ill-suited to competition

Ecological constraints, strategic and societal choices

One of the special features of the electricity system is the essential nature of the commodity it supplies, for both households and businesses: our society is totally dependent on energy.

Although electricity accounts for only a quarter of final energy demand, it is irreplaceable for certain uses. And this share is set to grow in the future. This is a necessity if we are to meet our climate commitments (carbon neutrality by 2050, which implies maximum use of low-carbon electricity) and for obvious geopolitical reasons.

France had opted to guarantee all its citizens fair access to this essential commodity through a single tariff grid. The aim was to avoid penalizing rural areas far from the network, in the interests of regional planning (known as “péréquation tarifaire”). 2 .

In addition, electricity generation generates major, protean ecological impacts that vary from plant to plant: greenhouse gas emissions and air pollution (for fossil-fired power plants), impact on biodiversity and landscapes, waste production, risk of major accidents, consumption of natural and agricultural areas, etc. The choice of production methods and our energy consumption patterns are also central to strategies for achieving carbon neutrality in the face of the climate emergency. The choice of production methods and energy consumption patterns is also at the heart of strategies to achieve carbon neutrality in the face of the climate emergency.

The power system is also subject to political choices relating to energy independence: to what extent do we accept dependence on imports, whether of fuels, other elements required for production (solar panels, batteries, equipment used in power plant construction) or electricity produced by other European countries interconnected to the French grid to meet our demand? And above all, is it acceptable to entrust the means of production to large private groups, whether French or foreign (bearing in mind that business law cannot guarantee that a French player will retain control of a private company)?

The electrical system is cooperative by nature

The power system is made up of a set of generation plants with complementary characteristics, as well as networks. 3 networks, which automatically deliver electricity to consumers in real time.

At any given moment, the total production injected into the network by the various power plants must be exactly equal to the sum of consumption drawn by users from this network. In the event of even the slightest imbalance (due to the failure of a power plant or line, or to an error in forecasting consumption or production), and without prompt action by the network operator 4 the whole of Europe can be plunged into darkness in a matter of seconds.

Each consumer therefore depends on the smooth operation of the entire European power system, and not just on the resources of his or her supplier. Each component of the system must cooperate closely with the others to maintain the overall balance, despite strong uncertainties (particularly meteorological) and the multiple constraints weighing on each power plant. Each one interacts in a complementary way, in consultation with the grid operators, and certainly not in competition.

Necessary planning

Ensuring this balance requires planning on all time scales.

In the long term, planning helps determine the investments required for production and network sizing.

The government’s adoption of long-term climate and energy objectives further reinforces the need for long-term planning to define a trajectory towards totally carbon-free power generation.

These are :

- guarantee that installed generation capacity will be able to meet forecast consumption, at all times and for all conceivable operating contingencies (weather conditions, failure of one or more power plants, etc.);

- size the network capable of carrying this energy, taking into account the location of production and consumption, and any damage that may also affect the network (lightning strike, tree falling on a line, etc.).

Within these technical constraints, several investment scenarios can be envisaged, and are subject to political arbitration based on economic criteria, as well as ecological, strategic and societal ones: acceptability of a given sector, independence of supply, environmental impact, etc.

Several energy scenarios (including or excluding non-electric energies) are drawn up to inform decisions on the investments required. At power system level, they provide a variety of technically possible futures.

The most important choice when it comes to energy lies in choosing one or other of these scenarios, not in choosing an electricity supplier or a more or less green offer (see section 4.C).

The organization of in-depth public debates on these scenarios is imperative in a context of international and local tensions. No energy source is without its drawbacks. Limiting energy consumption is generally costly and difficult, especially for the most disadvantaged who have the least access to alternatives. Our fellow citizens need to understand the ins and outs of major decisions, which commit France for decades to come and can create local nuisances.

Energy planning and forecasting in France

The National Low-Carbon Strategy (SNBC ) is France’s climate policy roadmap. It is the result of regularly updated foresight work. The latest version was published in April 2020, and recognized as legally binding by a Conseil d’Etat ruling in November.

Ademe has published energy transition scenarios for 2050, covering all energies and their uses, and assessing their environmental impacts (greenhouse gas emissions, material footprint, etc.). 5 ). Part of the work is regionalized. The results are expressed in the form of four scenarios: S1 “Frugal generation”, S2 “Territorial cooperation”, S3 “Green technologies” and S4 “Restorative bet”. This work is intended in particular to feed into the next version of the SNBC, due for publication in 2023.

RTE 6 has published several electricity scenarios for the year 2050, based on a number of generation mix assumptions designed to supply different levels of consumption. 7 . The SNBC is an input to these scenarios, which require hour-by-hour simulations of production and consumption over a range of long-term climatic assumptions. They are analyzed from economic (system costs), ecological (impacts on resources, waste, carbon footprint, air and water quality, land use, etc.), sociological (implications for lifestyles, acceptability) and technical (industrial risks, etc.) angles. They take into account current and potential interconnections with neighboring countries, and integrate the potential impact of climate change on electricity production, transmission and consumption.

The NegaWatt association has carried out an all-energy forecasting exercise, which also provides the carbon and material footprints induced by the options selected. The particularity of this exercise is that it is framed by the need to phase out nuclear power as quickly as possible, and to aim for the lowest possible energy consumption.

Source Learn more: Lessons from recent energy foresight studies, Chroniques de l’Anthropocène blog (2022)

In the medium and short term, the aim is to adjust electricity production and demand.

- In the medium term, planning is essential to coordinate the maintenance periods of the various production resources. 8 and to define strategies for using the water stored in hydroelectric dams 9 .

- In the short term, and right up to real time, the aim is to coordinate generation resources and the grid in such a way as to ensure a balance between electricity demand and generation at the lowest economic cost, taking into account the various technical and environmental constraints. 10 .

This planning on all timescales aims to make the best possible use of the complementarity of each power plant, in coordination with the grid, to guarantee the balance of the power system at all times, at the lowest economic, ecological and social “cost”.

RTE is responsible for 6 to guarantee the supply-demand balance at all times, with the support of the various producers.

On the other hand, it’s up to the State to decide on the trajectories, the means of production to be installed or renovated, and to put in place the regulations and systems that will enable this to happen in the long term.

Fixed, long-term costs

The power system, both the grid and the generating fleet, is essentially made up of fixed, long-term costs: these are the characteristics of a natural monopoly. 11 .

Production costs: fixed and variable costs

Fixed production costs, which are independent of the quantity of electricity produced, include the initial investment, part of the operating costs associated with maintenance, and end-of-life investments (decommissioning). These costs also include the cost of financing investments, i.e. the return required by investors and the repayment of interest on loans.

Variable production costs, which depend on the quantities of electricity produced: these are mainly fuels (coal, gas, uranium), but also waste treatment costs and the portion of operating expenses that increases with the quantities produced.

Full cost is the sum of fixed and variable costs.

All these costs can be calculated over the entire lifetime of the plant, based on one year (fixed costs are then “annualized”) or based on the Megawatt-hour produced (the full cost is then referred to as LCOE, or Levelized Cost of Energy).

There is a consensus that electricity transmission and distribution networks are natural monopolies.

Given their costs and environmental impact, it would be absurd to develop competing networks to supply a region, a town or a district. These networks are therefore entrusted to monopoly players. In France, RTE is in charge of the transmission network, while Enedis manages the distribution network for 95% of the country (around 150 local distribution companies). 12 for the remaining 5%).

Energy market promoters, on the other hand, do not recognize this characteristic for the generating fleet.

The “market launch” of the electricity system didn’t concern the networks, but the producers and suppliers of electricity. And history has shown that, in reality, it has only concerned a small link in the value chain, namely electricity supply (see part 4 and our fact sheeton the retail electricity market ). In the generation sector, the entry of new players has been extremely limited.

This was rather inevitable, as production costs in the nuclear sector are more than 80% fixed, and this proportion approaches 100% for renewable energies (hydro, wind and photovoltaic). These costs are largely linked to the construction of the facilities, which have very long lifespans: around 30 years for solar, wind or thermal energy, 40 to 60 years for nuclear power, and sometimes well over a century for hydroelectric power.

Finally, investment in the power system is very high. They have been in the past (around €13bn/year).

This will be even more the case in the future, in order to maintain and renew an ageing fleet of power plants, and to maintain and adapt networks to support the energy transition (around €20 to €25 billion/year). According to RTE, investments in generation account for around two-thirds of the total amount invested. 13 .

Under these conditions, for both generation facilities and grids, it is of course undesirable to build more generation facilities than necessary, simply to put them in competition with each other and keep only the “best”, i.e. those that produce at the lowest cost. All the more so since, like networks, they have a major impact on the environment, and the possible sites are limited by physical constraints and the acceptability of the structures. Nor, of course, is it desirable to under-invest, which could happen if the market price is insufficiently remunerative or too volatile.

Electricity is an undifferentiated product, and demand is not very adaptable to supply.

Once the generating facilities are built, the electricity delivered is the same for everyone

An electron remains an electron, and it’s not possible to guarantee consumers where their electricity comes from. 14 . The choice of type of generation (e.g. nuclear or 100% renewable) is made at the time the power plants are built. Some players see this as a way of differentiating the “electricity product”, through green offers that are supposed to guarantee 100% renewable origin, or more precisely, as an incentive to build renewable production facilities. As we’ll see in section 4.C, however, this is a false promise.

Nor can offers be differentiated on the basis of the quality of the electricity delivered (greater or lesser frequency of power cuts or voltage drops), since this depends on the network. 15 and the generation facilities connected to it, not the electricity supplier.

For more details on this point, you can also consult our fact sheet explaining just how little differentiation there is between electricity supply offers.

Electricity demand is not very price-elastic

Furthermore, the existence of a market depends on the ability of both supply and demand to adapt to each other: in theory, demand should fall when prices are high, and rise when prices are low.

Yet electricity demand is extremely constrained: for a household, it is difficult to significantly reduce or shift electricity consumption without worsening living conditions; for a company, a drop in electricity consumption would lead to a halt or shift in production, resulting in technical and/or economic difficulties. 16 . Conversely, consumers are not going to suddenly start consuming on a massive scale because prices are low.

Electricity demand is not very price-elastic: in the short term, a rise (or fall) in price does not translate into a significant fall (or rise) in consumption. In fact, consumption is largely determined by structural factors (hours of consumption depending on organizational constraints, better or worse insulation of homes, more or less efficient electrical and electronic appliances, production processes, etc.) which can only be changed over the long term, via investment in particular.

There are also solutions for adapting demand to production at the level of the power system itself. However, uses that can be shifted in time or “erased 17 are currently limited (certain industrial uses, and, for residential customers, the activation of hot water tanks, washing machines and dishwashers), and electricity can only be stored to a very limited extent: today, essentially in the form of water in dams, tomorrow possibly in the form of hydrogen or biomethane, and through the use of batteries, with the possible contribution of batteries for electric vehicles, which are set to expand rapidly. This is a real challenge, but it requires technological leaps, major investments and an organization of the power system that enables these levers to be effectively managed.

How did the opening up to competition come about?

Because of the specific features of the electricity system, a public monopoly (EDF-GDF) was set up after the war to manage electricity and gas in France. In other countries, various organizations were set up 18 most of them public, but with varying degrees of centralization depending on the country’s history, culture, organization, geography and available energy resources (coal in Germany, coal and gas in the UK, hydroelectricity in France, etc.). 19 . Exchanges between interconnected European countries were organized between national grid operators.

Since 1996, the electricity (and gas) sectors have been gradually opened up to competition. As we shall see, despite major changes in the way the system is organized, this competition remains fairly artificial. What’s more, it is driving up the system’s overall costs.

Opening up to competition has led to a profound transformation of the electricity system

In 1996, a European directive required all EU member states to set up an electricity market, considered to be :

particularly important for rationalizing the production, transmission and distribution of electricity, while strengthening the security of supply and competitiveness of the European economy and respecting environmental protection.

Competition is justified in particular by the objective of low prices.

If, in the face of market failure, some economists 20 now dispute this initial statement, European texts are clear on this point. For example, the first sentence of the European Commission’s website dedicated to the electricity market states: “An integrated European energy market is the most economically efficient way to ensure a secure and affordable energy supply for European citizens”.

The President of the European Commission, Romano Prodi, at the Barcelona European Council of March 15 and 16 2002, which marked an acceleration in the liberalization of the gas and electricity markets, also made this promise clear: “It is clear that this agreement will lead to a reduction in prices and an increase in competition”. 21 . He even went so far as to put a figure on the savings expected from these price cuts: “Full liberalization would result in annual savings of 15 billion euros in lower prices”. 22 .

As elsewhere in Europe, the organization of the French electricity sector has undergone a profound transformation.

- EDF and GDF were separated into two separate companies (one for electricity, the other for gas) and became private companies, in order to avoid benefiting from a public guarantee ensuring better financing conditions than their competitors.

- Network management, recognized from the outset as a natural monopoly, has been separated from the supposedly “competitive” generation and supply activities. Today, it is carried out by two EDF subsidiaries that must guarantee their independence from the parent company: RTE for the high-voltage network, and Enedis for the medium- and low-voltage networks. 23 .

- New players – producers but above all suppliers – have emerged, and markets have been set up to organize exchanges between them.

- An independent administrative authority, the Commission de Régulation de l’Energie (CRE), has been set up to ensure the smooth operation of the electricity and gas markets.

The electricity market has developed on two levels.

- The wholesale market, which organizes electricity trading between industry professionals (producers, suppliers and large industrial customers) via an exchange(see Part 3).

- The retail market, which represents all contracts between suppliers and end consumers (households, businesses, public authorities, etc.): commercial offers (known as market offers) and the regulated sales tariff offered by incumbent suppliers (EDF and local distribution companies, etc.). 12 )(see section 4). This is not a stock exchange.

Off-market competition for power generation

Once selected, producers are no longer in competition with each other.

To encourage the emergence of new producers, in the early years of the opening up of the electricity markets, the management of certain public production facilities was transferred to private players. Thus, part of the management of hydroelectric production on the Rhône was transferred to the Compagnie Nationale du Rhône (CNR), now a subsidiary of Engie. 24 .

Other means of production were developed by private investors. First there were combined-cycle gas turbine (CCGT) power plants, which were supposed to be paid for on the market, but for which support mechanisms had to be put in place. Then came privately financed wind and solar power plants. However, as we’ll see in part 3, wholesale market prices are highly volatile and far too uncertain for producers to take the risk of investing for the long term on the basis of this market alone.

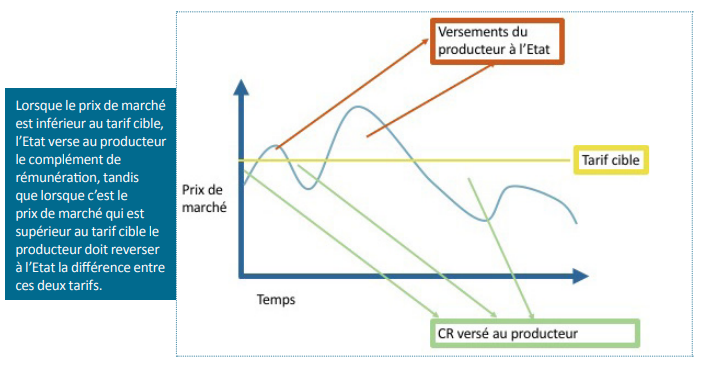

That’s why these new production capacities have been financed via non-market mechanisms, in the form of feed-in tariffs guaranteed for the entire life of the facilities, or remuneration supplements(see Appendix 1).

Investors thus benefit from a long-term contract with the State. Their situation is comparable to that of freeway, airport or water distribution operators.

The challenge of financing low-carbon energies

The cost of low-carbon energies is characterized by the high proportion of investment depreciation (CAPEX) and capital costs compared with operating costs (OPEX).

Indeed, the cost of fuel, which represents a significant proportion of operating costs, is zero for hydroelectric, photovoltaic and wind power plants, and low for nuclear power plants.

The cost of capital is a determining factor in the overall cost of electricity, as noted by David Newberry, one of the economists who theorized about deregulation of the sector in the UK: “All low-carbon technologies have costs that are extremely sensitive to their cost of capital”. 25 (see box).

The cost of investment financing: a key parameter

Given the predominance of fixed costs (and therefore investment), the total cost of the power system is highly sensitive to the cost of financing.

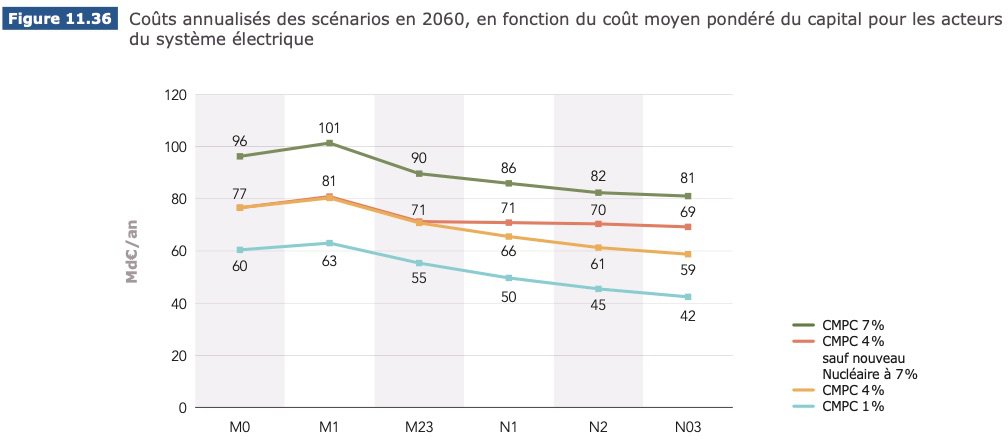

RTE’s “Energy Futures 2050” study highlights the importance of this parameter right at the start of the economic chapter: “For a variation in the annual rate of return on capital ranging from 1% to 7%, the full annual cost varies by more than €35 bn/year for all scenarios, an order of magnitude far greater than the differences due to the respective proportions of renewable and nuclear generation”.

Source : Futurs énergétiques 2050(chapter 11, fig.11.36), RTE

As shown in the graph above, the full annualized cost of the 100% renewable scenario (M23) is €55 bn per year for a financing rate (or CPMC _ weighted average cost of capital) of 1%, a rate that the French government can easily afford today. This rises to €90 bn/year for a rate of 7%, which is the typical rate demanded by private investors. This represents a 64% increase in the total cost!

The impact is of the same order for the reference scenario with nuclear power (N2), whose cost rises from €42 to €91 billion (+82%) when the financing rate (CPMC) is increased from 1% to 7%.

What’s more, when renewable energies were launched, they were still immature and required subsidies for their development. The free functioning of the market could not help them to emerge. 26 . Similar questions about financing arise today for nuclear power (with the new EPRs), as well as for new hydroelectric facilities whose cost price may be higher than the market price of electricity.

The French government has therefore put in place non-market instruments to enable the deployment of renewable energies. Feed-in tariffs for wind and solar power guaranteed developers long-term returns. At the same time, a global dynamic led to considerable reductions in the cost of renewables. As a result, we have seen significant over-remuneration, as noted by the Cour des Comptes in a report on support for renewable energies in April 2018. These initial feed-in tariffs still weigh in part on consumers’ bills, despite substantial modifications to the arrangements (see Appendix 1).

It should be noted here that the cost of capital theoretically serves to remunerate the “present preference” and risk-taking of the financier. However, we need to distinguish between two types of risk: the commercial risk (of unsold power or of selling at too low a price in relation to costs)-which can be eliminated with guaranteed tariffs and/or additional remuneration-and the industrial risk (of construction, risk of cost overruns or excessive delays), which is particularly sensitive in the case of nuclear power.

Growing industrial expertise and price guarantee mechanisms have enabled renewable energy developers to reduce the cost of capital. Until 2020, renewable energy projects were still being financed with a Weighted Average Cost of Capital of less than 27 than 5% (with 3/4 borrowed at ~3% and the remaining 1/4 financed by equity at ~10%). This, of course, still weighs on the cost of the electricity produced, especially as the initial capital is remunerated over the entire operating life of the project, not just the construction period.

It should also be noted that the new EPRs, in view of the cost and schedule drift observed for the first ones (Olkiluoto and Flamanville, but also to a lesser extent Hinkley-Point), appear to be industrially risky. For a private player, financing them would require a higher, even prohibitive, cost of capital, unless a state guarantee were to be put in place.

To conclude on this point, it is clear that the construction of low-carbon power plants cannot be achieved by relying on market mechanisms alone.

Should competition apply to plant construction and operation?

Apart from existing nuclear and hydroelectric power plants, developers of power plant projects are not necessarily the operators. Nor are they necessarily the builders.

In the nuclear sector, while the current fleet was built and is operated by EDF, the technology was put out to tender: Westinghouse won out over General Electric and CEA.

This means that competition in generation technologies, plant construction and maintenance services does not mean that the operation of these plants has to be managed by competing players, nor, above all, that investments have to be remunerated over the entire lifetime of the plant.

Inviting tenders not only for the construction of the park, but also for its operation, is likely to lead to a number of problems:

- This significantly increases the cost of production: the investor who responds to the call for tenders will not be reimbursed on delivery of the plant (at the end of the construction phase), but progressively over its entire operating life, via guaranteed tariffs or similar mechanisms. It therefore acts as a lender to the community over a very long period, and is remunerated at a higher rate than a public loan.

- For controllable controllers 28 management by a single operator allows better optimization of the call program.

- Strategically, and for reasons of democratic control, it seems preferable not to depend on the decisions of private French or foreign players for production as sensitive as that of electricity. 29

In addition, competition in the upstream construction phase of a wind farm does not obviate the need to consider the national and European strategy that needs to be put in place to manage these activities (wind power, photovoltaics, storage, etc.). 30 (see section 5). This can be achieved through the development of industry sectors, under the impetus of the government, which is in a position to organize these sectors (in particular through research, training, skills development, etc.).

The electricity supply business was created for the purposes of competition.

Financial and commercial activity, marginal and useless

Before the market was opened up, EDF billed all French consumers for the electricity it generated, transmitted and distributed (except for the 5% of the territory served by local distribution companies). 12 .

Today, in addition to the incumbent suppliers (EDF and ELD), the French retail market includes some 80 so-called “alternative” suppliers (40 of which are for residential consumers).

These include foreign electricity companies (Vattenfall, Iberdrola, etc.), oil companies (ENI, Total Energie), gas companies (Engie, formerly GDF), start-ups, retail chains (Carrefour, Cdiscount, etc.) and militant cooperatives (Enercoop). 31 . These alternative suppliers bill electricity to around 12 million sites (including 10 million residential sites).

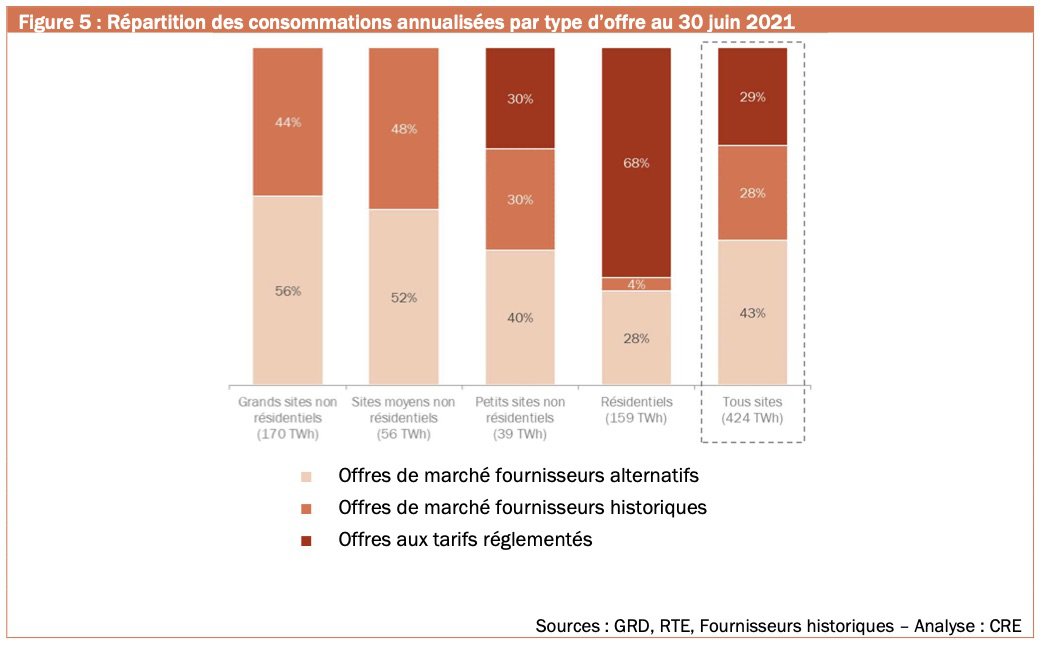

As the following chart shows, alternative suppliers account for 43% of the total volume of electricity sold in France, with a stronger presence in the very large customer segment (electro-intensive businesses) and a weaker presence in the residential sector.

Market share of EDF and alternative suppliers by type of offer and type of consumer

Source Observatoire des marchés de détail du 2e trimestre 2021 – Commission de régulation de l’énergie (CRE)

Suppliers buy electricity from producers and sell it to consumers. They are not involved in the technical side of the business, nor do they “touch” electricity production. 32 or its transmission to the consumer. As we have seen, electricity is transmitted automatically, with no possibility for suppliers to intervene: in particular, they cannot choose which generation plants will supply their customers. Nor do they store electricity or read meters (this is done by network operators).

Suppliers are limited to acting as financial and commercial intermediaries between producers and end consumers. They draw up sales offers, canvass customers, buy on the wholesale electricity markets, and issue invoices to their customers (generating re-invoicing by network operators for the part of the invoice linked to network use).

Supply activity adds cost and complexity to the power system

Before the opening to competition, there was no trading, canvassing or marketing, since the monopoly producer EDF sold electricity directly to all users, according to a single, simple price scale, set to cover the overall production costs of the electricity system(see section 4).

Many of the activities carried out by suppliers therefore result in additional costs for the power system: creation of commercial and trading functions (to buy electricity on the wholesale market), duplication of support functions (billing, administration, consumption forecasting, etc.) at each supplier, transaction costs linked to the contractualization of exchanges, and so on. These additional costs are, of course, passed on to the end consumer.

On the other hand, the customer relations provided by the public service in the past have deteriorated (whatever the type of consumer, but particularly for the most vulnerable): agencies providing a physical welcome have disappeared; neutral information has given way to particularly aggressive marketing and commercial canvassing, regularly denounced by the Energy Ombudsman and consumer associations. 33 Consumers are tossed back and forth between Enedis, for network-related problems, and EDF or another supplier for contractual issues. Precarious customers receive less support and are less aware of the assistance available to them. For industrial customers, professions that used to involve highly specialized knowledge of electricity-intensive uses (e.g. arc furnaces) are tending to disappear(see section 5).

The wholesale market poses many problems

The emergence of new players (producers and suppliers) necessitated the creation of an exchange: the wholesale electricity market, which defines an exchange price between these players.

The wholesale market is also supposed to ensure coordination between these players to guarantee the balance of the power system from the short term (making the right operational management decisions) to the long term (making the right investment decisions over several decades), even though markets only exist over a three-year horizon.

Highly volatile wholesale prices

Electricity generation facilities are called up according to the merit order principle (which pre-existed the market).

At any given moment, we need to define the production plan for all power plants, known as the call schedule: this is the quantity of electricity to be produced by each power plant to meet electricity demand at the lowest cost, on the entire interconnected European grid.

The calling program is determined according to the economic “merit order” principle, in compliance with all technical and environmental constraints. 35 power plants are called up in ascending order of variable cost. Indeed, once investments have been made, fixed costs are no longer taken into account, since they can no longer evolve (they do not depend on operational decisions linked to the running of the generating fleet). The only possible lever for reducing system costs is therefore to minimize variable costs, which are the only ones that depend on the quantity of electricity generated.

The power plant with the lowest cost is called first, and so on: non-storable renewable generation with a variable cost of zero (photovoltaic, wind and run-of-river hydro) is therefore called first, followed by nuclear power plants and then gas and coal-fired power plants. 36 . The water in hydroelectric dams, whose cost is zero but whose quantity is limited, is assigned a fictitious value that makes it possible to decide whether it should be turbined to produce today, or stored to produce in the future. 37 .

Determining this call programme is a highly complex task. It requires a fine-tuned vision of the entire fleet, due to the many constraints weighing on the power plants, which bind them together, or which make it necessary to manage stocks (of water in dams, but also of fuel in nuclear power plants, or of demand-side shaving potential, etc.). 38 ) in an uncertain future, as they are highly dependent on climatic conditions.

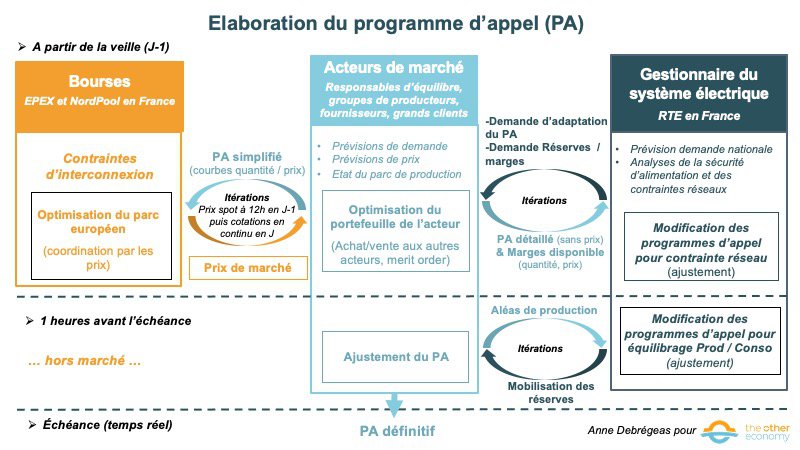

Preparing the call schedule, from the day before (D-1) to real time

Source L’auteur

Wholesale electricity prices are based on marginal cost, making them highly volatile.

The wholesale market price is equal to the cost of increasing consumption by 1 MWh at a given time: this is known as the marginal cost. This cost corresponds broadly to the variable cost of the last (i.e. highest) power plant called on the interconnected European grid, known as the marginal cost of production. As this is often a gas- or coal-fired plant, this marginal cost depends largely on the cost of the gas or coal fuel. 39 the main variable cost component for these plants. 40

This is why, although the price of gas accounts for only a small proportion of the total cost of electricity generation (around 7% in France or Germany), its wholesale price is mostly dependent on it, making it highly volatile and difficult for the public authorities to control.

Definitions

Wholesale prices are the prices governing exchanges between professionals on the wholesale market. They cover different types of prices (intraday, spot and forward), depending on the time between purchase and delivery of the electricity.

Spot price: refers to the price of electricity purchased for next-day delivery.

Forward price: refers to the price of electricity purchased for delivery over a longer period, between 1 month and 3 years after purchase. The most common forward price, and the one most widely used as an index to establish the selling price to consumers, is the purchase price for calendar delivery (the whole year) following the purchase (called Year Ahead).

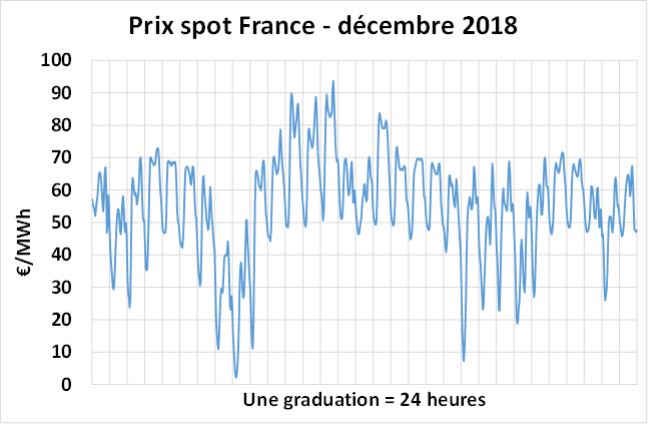

Spot prices can fluctuate from 0 to several hundred or even thousands of euros per MWh, depending on delivery times.

Spot price trend in a “normal” winter month (December 2018)

Source EPEX

Reading: during December 2018, the price of a MWh quoted the previous day varied between around €0 and €90/MWh depending on the time of delivery.

The forward price represents the purchase of 1 MWh for future delivery, over a timeframe ranging from one month to several years. This price is likely to be very stable, since it is not impacted, a priori, by cyclical hazards (weather or power failures) and average annual electricity demand changes little (except for the particular period of 2020 linked to Covid).

However, this price is also highly volatile, albeit to a lesser extent, as shown in the graph below.

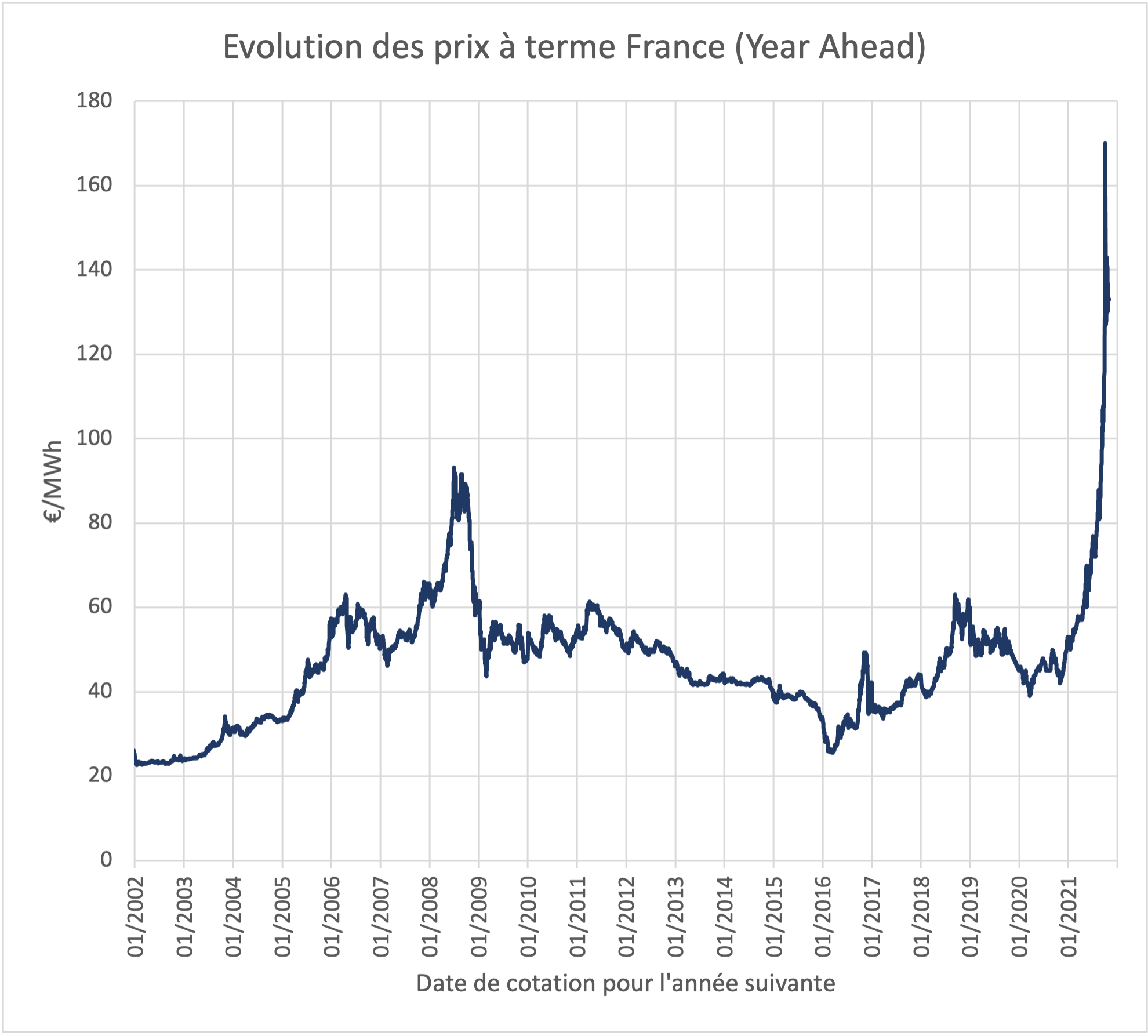

Forward prices have varied between around €20 and €170/MWh over the period presented (2002-Oct 2021). They even exceeded €250/MWh in December 2021.

At the same time, production costs have changed very little (see graph below on the breakdown of power system costs).

Year-ahead prices in France from 2002 to 2021

Source EPEX

Reading: on January 1, 2016, the purchase of 1 MWh for each hour of 2017 was priced at around €26/MWh. On October 3, 2021 (for delivery in 2022), it was €170/MWh.

Volatility is highly correlated with that of fossil fuels. The graph above shows the effect of rising commodity prices (fuel and CO2 prices) up to 2006; then the bursting of the European CO2 bubble, causing prices to plummet; then the surge in fuel prices in 2008, largely linked to the Beijing Olympics (causing tension on freight); then the collapse due to the 2008 financial crisis; then a further rise in commodity prices from 2009 to 2012; then the fall in prices induced by the discovery of American shale gas until 2016. ; followed by a further rise in coal and gas prices, until the recent gas crisis at the end of 2021, linked to the post-Covid global recovery and problems with Russian gas supplies to Europe.

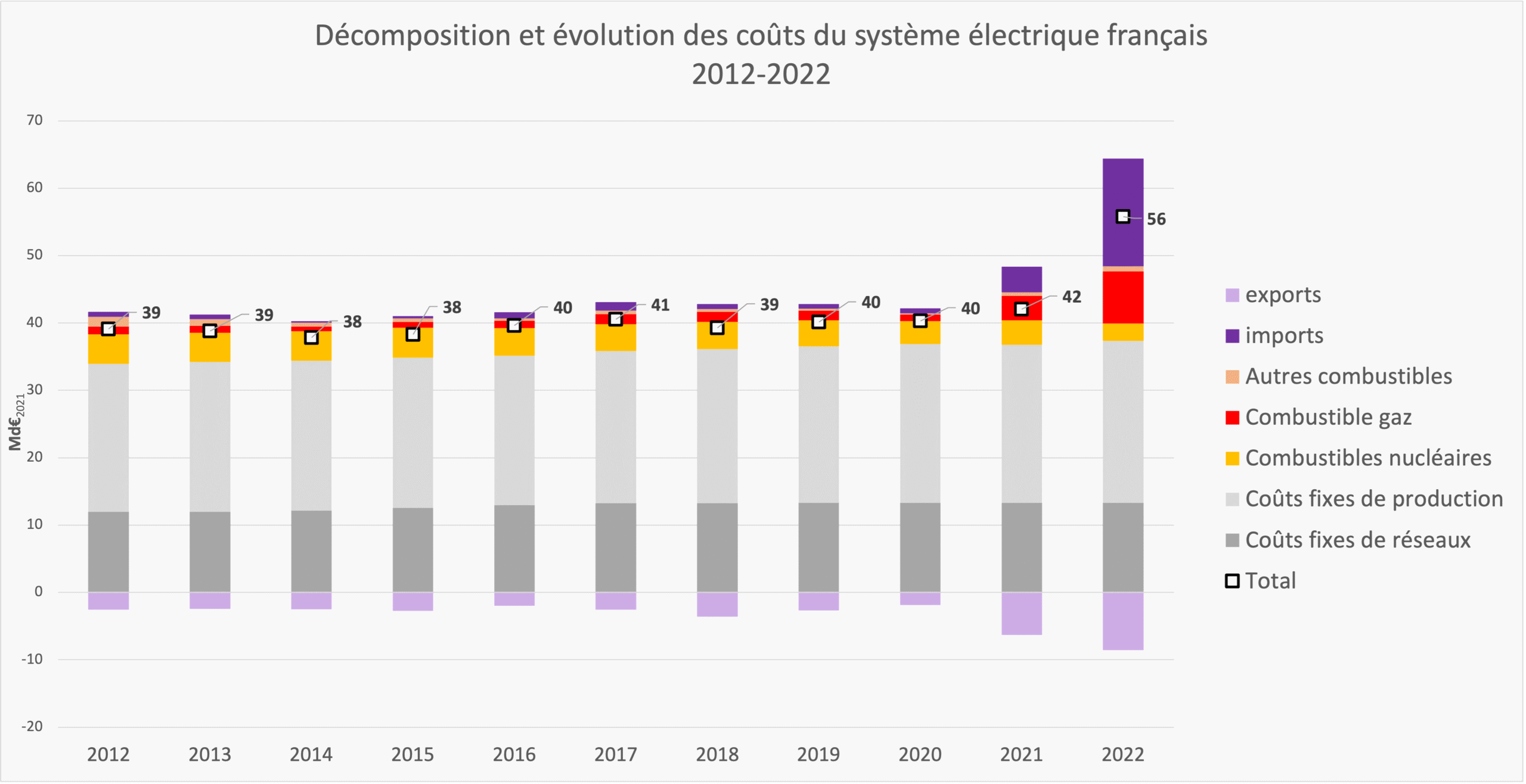

Breakdown and evolution of French power system costs (generation and grids) 2012-2021

Source Author’s calculations based on AIE, SER, EDF, RTE, CRE, Observ’ER, EPEX/EEX. Download the excel file used to make the calculations.

In the long term, the market provides neither the visibility nor the returns required for investment.

As electricity production costs are largely made up of heavy investments amortized over several decades and fixed operating costs, it is imperative for the investor to have visibility on revenues throughout the amortization period.

In practice, investments in the electricity system are planned outside the market.

First of all, it’s important to remember that energy choices not only have an economic dimension, but also other criteria that are at least as important: ecological, geopolitical, industrial, societal and so on.

Investments are therefore the result of planned political decisions, based on long-term scenarios that guarantee the balance of the power system(see section 1). They are not market-driven, any more than they were in the past. 41 . For example, hydroelectric plants were built to the maximum available capacity; nuclear power plants were developed primarily in the name of France’s energy independence. 42 and wind and solar power are designed to diversify non-carbon sources alongside or in place of nuclear power.

The market is not able to take into account the diversity of these criteria, especially as it does not provide any visibility beyond 3 years, the maximum timeframe for quoting futures products on the existing wholesale market. 43 .

The market price is insufficient to finance the investment

At first glance, it may seem incomprehensible to have thought that the market price, based on marginal cost, would be capable of remunerating each plant at its fair value, i.e. covering both its fixed and variable costs (including a reasonable margin). This is a prerequisite if the market price is to provide the right incentive for investment, and tend towards an economically optimized system.

This property stems from an economic theory 44 which postulates that, under certain conditions, marginal costs are indeed equal, on average, to the full costs of each means of production. For example, over an average year, when nuclear power plants are in operation, they are remunerated at a marginal cost that is most often equal to the variable cost of gas-fired power plants. This enables them to remunerate not only the variable costs of nuclear power, which are much lower than those of gas-fired plants, but also – thanks to the difference between the marginal cost and the variable cost of nuclear power – the variable costs of gas-fired plants. 45 fixed costs (including depreciation and investment financing).

Unfortunately, this theory is very fragile, since it assumes that system costs, which are essentially fixed and long-term, will be covered by remuneration based exclusively on the variable cost of peak generation. Above all, the assumptions on which they are based are inapplicable in a market environment, whatever the composition of the generating fleet (see Appendix 3). Finally, wholesale prices are disconnected from power system costs, and unable to guarantee generators a return on their investment. For example, in the early 2010s, several producers invested in gas-fired power plants in Germany; a few years later, as a result of falling market prices and the inversion of costs between gas- and coal-fired generation (the latter once again becoming the cheapest), they were forced to “mothball” these brand-new plants, i.e. shut them down to at least avoid fixed operating costs.

The failure of the market to guide investment is now widely recognized 46 . This is why, over the years, various market bypass mechanisms have been put in place to provide visibility and guarantees for producers: guaranteed feed-in tariffs or contracts for difference, long-term contracts, complementary markets, etc. These are just a few examples. 47 (see Appendix 1).

The European Commission constantly criticizes these mechanisms as distortions of the free play of competition, but is forced to come to terms with them every time, given the extent of the market’s malfunctioning. Moreover, these mechanisms for circumventing the market are not exclusive to France: even the very liberal United Kingdom, for example, has introduced long-term contracts in all production sectors.

Some economists see the wholesale market’s inability to finance investment as a consequence of the development of intermittent renewable energies – solar and wind – whose zero variable cost is particularly at odds with theory. In reality, this major dysfunction concerns all production sectors. No new power plant can be built if the investor has to be remunerated by a market price that is highly volatile and disconnected from the full costs of production (mainly made up of fixed costs). The same applies to the capital-intensive balancing facilities required for the energy transition, such as hydroelectric pumping stations (STEP) and electrolysers for hydrogen production (see Appendix 1).

In the short term, the market is less efficient than an integrated system

While there is a consensus that the market fails to promote the right investment decisions, many economists continue to attribute to it the ability to effectively coordinate the various means of production, in order to define at any given moment the optimal production program, i.e. at the lowest operating cost. The market thus retains its role as short-term coordinator.

First of all, it should be noted that in a system where fixed costs account for almost 80% of the total, short-term coordination represents a limited, if not negligible, challenge. Above all, both theory and practice show that market coordination is less effective than coordination by a single operator.

Market coordination less economically efficient than a single player

As we saw in section 3.A, whatever the organization of the power system, plant production plans (call schedules) are defined according to an economic merit order, in ascending order of variable cost.

Prior to deregulation, EDF carried out this short-term coordination by merit order, using optimization programs that took into account the many constraints and hazards affecting the generating fleet in order to determine the optimum call schedule.

In a system where there is no longer a single operator, but rather a group of producers and buyers (suppliers), each player has only part of the information at their disposal, and coordinates via the market. The general optimization problem previously solved by the single operator therefore undergoes a “price decomposition”, so that each actor is assigned a sub-problem. However, due to the nature of the constraints 48 on the generating fleet, this multiplication of players systematically degrades the calling program and drives up costs, even in an ideal situation where the market price would be “perfect” and all players would play a fully virtuous game for the community, i.e. seek to minimize the full cost of electricity (which is far from being the case in reality, see next point).

This result is widely documented in the scientific literature 49 but is also supported by practical experience: players with large fleets don’t determine the call schedule for their fleets by simply simulating a market 50 .

In short, centralized optimization by an efficient, integrated player delivers better results than a perfect market, let alone the real thing.

Recourse to the market multiplies the risk of abuse of a dominant position

Some advocates of competition point to the danger of a concentration of resources in the hands of a single player who could exercise market power, i.e. manipulate prices to his own advantage and to the detriment of consumers. We note that this fear is not backed up by any concrete examples, despite the numerous case studies of electricity systems managed by public monopolies.

Analysis of numerous foreign examples 51 including the emblematic Californian disaster of 2001, shows that the multiplication of private players does not prevent them from exercising strong market power. Given the technical characteristics of the electricity system, the failure of just a few generating units is enough to jeopardize the entire network during periods of high consumption: if a player refuses to produce, there is a risk of blackout, and prices soar.

The question arises, however, in the more complex case of France’s integration into a European “plate”. This centralized optimization could not be left to EDF. We’ll come back to this point later (in the paragraph on European coordination).

The fiasco of electricity market liberalization in California (2001)

In California, liberalization was implemented in 1996: the two incumbent producers were forced to sell off their production facilities, allowing seven private producers to emerge. Companies specializing in energy trading (purchase for resale on the markets and speculation on stock market prices) sprang up, such as Enron.

The ensuing near-total halt in investment, and above all the manipulation of market prices by producers who “held back” their production on the pretext of unavailability, created artificial shortages that sent prices soaring and put distributors in difficulty.

This crisis led to 38 days of rolling blackouts in California, a 40% increase in electricity rates, a 35% reduction in the number of employees in the electrical industry, a $45 billion loss for the State of California between 2000 and 2001, and the placing of this state, the richest in the United States, under surveillance by the financial community, a treatment generally reserved for developing countries.

Finally, the Californian state had to step in for distributors threatened with bankruptcy and buy electricity at exorbitant prices under long-term contracts running until 2011. This unfortunate experience put a stop to the liberalization experiment in 23 US states.

Source The Californian experience is recounted in detail in François Soulte’s book EDF Chronique d’un désastre inéluctable (2003) and Gilles Ballastre’s documentary Les apprentis sorciers (2005), which features interviews with Californian electricity players (see a transcript of these interviews here). You can also read this twitter thread dedicated to the Californian disaster.

To prevent such manipulation, we need to keep a very close eye on the producer, as the Commission de Régulation de l’Energie is doing today with EDF. 52

We can also envisage entrusting production to a player whose primary objective is to provide a service mission, as is the case with companies with public status. EPIC (Établissement Public à Caractère Industriel et Commercial) status, for example, requires that all profits be reinvested. The company has no interest in manipulating the market.

Is national de-optimization offset by better European coordination?

Has the opening up of markets led to better coordination between countries? Has it led to lower operating costs that could more than offset the national de-optimization discussed above?

While the interconnection of the European network long predates the introduction of markets, it’s true that coordination between countries has improved over the last few decades. But is this improved intra-European complementarity attributable to the market?

Geopolitical factors, such as the fall of the Berlin Wall, and technical factors, such as the development of intermittent renewable energies, which make it increasingly necessary to pool peak load resources and the “proliferation” of consumption, may also explain this development, which began in the era of public monopolies. It should also be noted that methodological progress in the management of exchange capacities between European countries via interconnection lines is not linked to market regulation of the European power system.

The rules of the European market mean that each country accepts to lose some control over the operation of its generating fleet, in order to submit to the call program coordinated at European level by the stock market operators. It becomes impossible, for example, for a country to give priority to the operation of a national power plant for reasons of economic balance or local employment, or on the basis of ecological criteria that would contravene the merit order. 53 . In return for this loss of sovereignty, the optimized European call schedule makes the best possible use of the complementarity of generation resources and the abundance of demand between different countries, via interconnections. 54 .

However, just as at national level, the market is not the best solution for short-term European coordination. A centralized public optimizer at European level would be the best solution. 55 which would apply collectively-defined merit oder rules and have visibility over information on the different means of production, could do a better job than the market.

Optimizing the operation of generation facilities on a European scale therefore does not in itself require the creation of a market, with its attendant perverse economic, social and democratic effects.

Finally, it should be remembered that the introduction of electricity markets is only intended to ensure short-term coordination of the European fleet (i.e. its operation), and not to plan and coordinate investments. However, it is the latter that is the most important in terms of cost (see section 1.D). Coordinated investment planning on a European scale, while respecting the constraints specific to each country (e.g. choice of technology, preservation of a certain level of energy independence), would therefore have a far greater impact, and would make it possible, for example, to pool peak resources.

The retail market: the impossible equation between the need for price stability and the market

What is the retail electricity market?

As we saw in part 2, the opening up to competition has introduced new intermediaries, suppliers, whose role is to buy electricity on the wholesale market from producers and resell it to consumers. 56 .

The wholesale market refers to the exchange between electricity professionals (in particular suppliers’ purchases from producers). It’s worth noting that a large proportion of exchanges escape the market: on the one hand, because EDF, which holds around 80% of production and almost 60% of customers (in terms of volume sold), supplies its customers largely through its own production, without going through the markets; on the other hand, because alternative suppliers can access part of the nuclear electricity produced by EDF at the regulated price of €42/MWh through a market bypass mechanism, ARENH (Accès Régulé à l’Électricité Nucléaire Historique, see part 4.C).

The retail market refers to contracts between suppliers and end consumers (individuals or businesses). Unlike the wholesale market, it is not organized like a stock exchange, since it operates via bilateral contracts.

Whatever the type of contract, the electricity bill paid by consumers breaks down into three major cost items, of equivalent importance for a domestic consumer:

- TURPE (Tarif d’Utilisation des Réseaux Publics d’Électricité), a regulated tariff set by the French energy regulator, covering the cost of access to the transmission and distribution network.

- The energy share is intended to cover the costs of producing and supplying (or marketing) electricity.

- Taxes and contributions set by the public authorities (including, in particular, additional remuneration for renewable energies) 57 .

Suppliers therefore only set the price of the energy part of the bill, which is the only part “in competition”.

From theory to reality

In theory, the energy portion of electricity bills should perfectly reflect wholesale prices, in order to pass on to consumers the market’s supposedly optimal pricing incentives. This is the principle of dynamic pricing promoted by the European Commission (see appendix 2), one of whose aims is to meet the power system’s need for flexibility by encouraging consumers to shift their consumption to less peak hours.

However, to date, consumers do not have the means to significantly adapt their consumption to real-time prices, unless they jeopardize their business for companies, or go without heating and basic uses of electricity for private individuals: they can only shift a few uses, for example, hot water tanks and washing machines (to be started at night or midday rather than at the end of the day). Incentives to shift this type of use have existed for decades in the form of “off-peak” tariffs. 58 . It is entirely possible to further improve the adaptation of demand to production that is set to become more intermittent (wind and solar power), without seriously penalizing consumers or exposing them to the extreme volatility of wholesale market prices, by using “abundance”. 59 of consumption. This implies seeking the overall balance of the power system (which is what an integrated player would do), rather than individual opportunities for each supplier.

While dynamic pricing is not (yet!) the norm, we will see that liberalization of the electricity market has resulted in a shift from a system where retail prices based on production costs were relatively stable, to a system where retail prices are increasingly indexed to wholesale market prices.

The majority of consumers (individuals and businesses) find themselves exposed to market prices, whose volatility (see section 3.A) is incompatible with their need for price stability for the essential commodity of electricity.

Faced with the difficulties caused by this volatility in market prices, workaround mechanisms have been put in place to dampen fluctuations. These shock absorbers are more or less developed in different countries, which goes a long way towards explaining why the surge in gas prices in 2021, which was reflected in wholesale electricity prices in all European countries, did not have the same impact on consumer bills everywhere.

Historical operation: regulated sales tariffs (TRV)

Before the market was opened up, only the incumbent operator supplied electricity to consumers. All consumers had access to the same tariff grid: green tariffs for large consumers (industrial), yellow tariffs for medium consumers (small industries and tertiary businesses), professional blue tariffs for small businesses, and residential blue tariffs for individuals. In each category, prices depended on the level of subscribed power and options reflecting their consumption profile, offering a good compromise between price stability and incentives to consume at times most convenient for the power system. 60 .

These tariffs were calculated to cover, on average, all production costs (including fixed costs) as well as transmission and distribution costs.

Each year, tariffs were adjusted in line with electricity system costs. As these costs were not likely to change abruptly, the trend was moderate, guaranteeing a degree of stability.

In a 2019 note, INSEE states: “After this counter-shock [1986], the nominal price of electricity evolved very moderately until 2007 (+2.6% between 1986 and 2007). This relative stability can be explained first and foremost by the commissioning of numerous nuclear power plants during the 1980s: electricity production costs are disconnected from fluctuations in hydrocarbon prices.” 61

Opening up to competition and diversifying electricity supply offers

The introduction of market offers and the abolition of regulated sales tariffs for businesses

The opening up to competition has meant that consumers can “choose” their suppliers and opt for different types of contract.

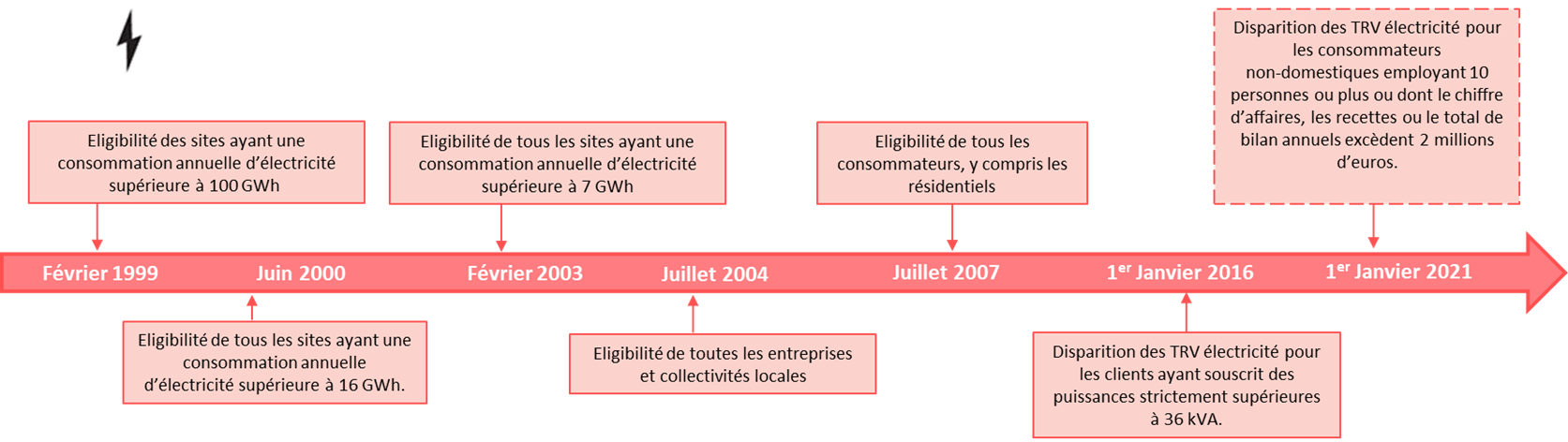

Opening up the market has been a gradual process, starting in 1999 with the largest customers, followed by smaller and smaller companies until 2004. In 2007, it was opened up to domestic consumers.

The steps involved in opening up the French electricity market to competition

For businesses, regulated sales tariffs initially coexisted with market offers. But customers who decided to leave the regulated tariffs had no right of return. Now, trapped by soaring wholesale prices that were threatening their financial health, in 2007 companies obtained from the legislator a right to return in return for a penalty of 20 to 23% of the initial tariff.

In 2007, at the instigation of alternative suppliers, the European Commission opened a State Aid procedure against France, with the aim of abolishing the TRV and return tariffs. These mechanisms are being challenged on the grounds of unfair competition, since, as Electrabel wrote: “Almost all Electrabel customer sites have asked to benefit from the return tariff. The return tariff has led to a gradual displacement of alternative suppliers in favor of EDF, since customers often prefer the latter for the same price”. 62 .

The French government reacted to this procedure by creating Regulated Access to Historic Nuclear Electricity (ARENH _ see next section) and by phasing out all regulated sales tariffs for businesses, which has been in place since 2015 (with the exception of very small businesses). Companies have therefore been forced to “choose” market offers.

Domestic customers and very small businesses continue to have access to the blue tariff, but only for a temporary period. 63 . They can choose between :

- The regulated sales tariff, set by the public authorities and still offered by the incumbent suppliers (EDF and the local distribution companies), is the only way to reduce the price of electricity. 12 ), but with major changes in the way they are calculated (see below).

- Market offers, proposed by all suppliers (alternative and incumbent) within the framework of contracts. These can be either fixed-price offers (where the price, excluding taxes, remains unchanged for the duration of the contract) or indexed-price offers (where the price follows changes in regulated sales tariffs or wholesale market indices specified in the contract).

ARENH (Regulated Access to Historic Nuclear Electricity): a non-market mechanism to stimulate competition!

In response to the state aid procedure initiated by the European Commission in 2007, France introduced a mechanism called ARENH in 2011. Due to expire in 2025, this mechanism requires EDF to make available to its competitors at a fixed price (€42/MWh corresponding to an estimate of the cost of production) around a quarter of its nuclear production (i.e. 100 TWh), corresponding to their market share in 2011.

The stated aim of ARENH is to put an end to the unfair competition that alternative suppliers would face from EDF, since the public operator benefits from the low-cost production of the historical nuclear fleet, which has been largely amortized. By giving alternative suppliers access to part of this production at cost price, ARENH would encourage competition in the supply business while competitors develop new production capacity.

How does ARENH and the capping mechanism work?

Under the ARENH scheme, EDF is obliged to sell up to 100 TWh to its competitors each year at the fixed price of €42 MWH, which is supposed to represent the production costs of the historic nuclear power plant.

In November, alternative suppliers submit their requests for ARENH volumes for the following twelve months to the Commission de régulation de l’énergie. They do so on the basis of their customers’ forecast consumption during low-consumption hours (known as “ARENH Hours”).

If overall demand exceeds the statutory ceiling of 100 TWh (as has been the case since 2019), the Commission de Régulation de l’Energie (CRE) will 64 must then proceed to capping ARENH volumes: after examining the validity of requests, it proportionally distributes the 100 TWh available. For example, during the November 2021 auction for the 2022 delivery year, the CRE received around 160 TWh of ARENH requests: after capping, each alternative supplier was allocated 62.37% of the volume requested, and will have to purchase the missing volumes directly on the wholesale market.

Source For more information, visit the EDF website or the CRE website.

ARENH is an asymmetrical mechanism.

Up to 100 TWh 65 alternative suppliers have the choice of either purchasing at cost (i.e., at the ARENH price of €42/MWh), or on the wholesale market when the latter falls below cost. The mechanism also offers them opportunities for speculation. For example, when prices were low in 2016, some alternative suppliers bought forward on the wholesale market, then resold at a higher price when prices rose in 2017, relying on ARENH to supply their customers.

Producer EDF, for its part, finds itself in a difficult situation, obliged to sell at a loss when the market price collapses (as, for example, in 2016, when it remained around €30/MWh for over a year) and to sell at cost price (at ARENH) when market prices are above €42/MWH. Of course, EDF argued that this mechanism was a drain on its finances and hampered its ability to invest.

On the consumer side, ARENH has acted as a powerful shock absorber against price rises on the wholesale market. Indeed, the regulated sales tariffs, which serve as a guide for other offers and today reflect the supply mode of alternative suppliers, include ARENH to a large extent in their calculation, reducing the proportion indexed to the wholesale market (see next section).

ARENH is the subject of much criticism from all players. Debates revolve around several points:

- The price: EDF has long been calling for an increase in the €42/MWh price, which was set in 2012 and has not been reviewed since. However, it is difficult to form an opinion on the reality of nuclear production costs, as they are so opaque.

- The asymmetrical aspect of the mechanism: rarely highlighted, this aspect is the most dangerous and penalizing for EDF (and therefore ultimately for consumers and taxpayers);

- The volume accessible to ARENH (100 TWh excluding the exceptional 2022 measure): supported by the Commission de régulation de l’énergie (CRE), alternative suppliers are calling for this volume to be increased, as it has not changed since 2011, even though their market share has increased;

On a more general note, everyone agrees that ARENH has not led to the emergence of any significant new means of production, and that suppliers are no closer than before to experiencing “free and undistorted competition”. Unsurprisingly, the mechanism has failed.

Finally, the situation is becoming increasingly untenable: the fact that the ARENH volumes requested by suppliers are capped a little more each year to meet the overall 100 TWh cap has a negative impact on consumers. This is because alternative suppliers have to buy the capped volumes on the wholesale market, which has an impact on the prices paid by consumers. 66 . On the other hand, increasing ARENH volumes, as requested by the French Energy Regulatory Commission, would mean agreeing to maintain under perfusion suppliers whose added value for the power system and for consumers is still being sought.

Changing the calculation of the regulated sales tariff to make room for competition

As soon as the electricity market was opened up, alternative suppliers attacked the TRVs, which were challenged by the European Commission as an obstacle to competition.

After obtaining their abolition for business customers, they obtained a complete overhaul of the method for calculating the regulated sales tariff for private customers.

Thus, since 2015, it has no longer been calculated on the basis of the incumbent operator’s production costs, but to approximate the supply conditions of an alternative supplier without production facilities. The energy portion of the tariff therefore reflects:

- The cost of the regulated nuclear price (ARENH at €42/MWh), for around 50% of the energy share.

- The wholesale price smoothed over two years for around 30% of the energy portion.

- And since 2019, the December wholesale price (for delivery the following year), corresponding to the ARENH capped volume (around 20% in 2021) 67 .

This method of calculation pursues the objective of “contestability”, defined by the Commission de régulation de l’énergie as “the ability of an EDF competitor present on or entering the electricity supply market to propose offers on this market at prices equal to or lower than the regulated tariffs”. 68 .

The aim is therefore to ensure that the TRV is high enough to allow competing offers from alternative suppliers. The stated aim is no longer to ensure supply at the best price for the consumer, but to enable alternative suppliers to offer a cheaper deal than the incumbent supplier. The texts thus explicitly organize the artificial increase of the TRV, when market prices are high, with the sole aim of enabling alternative suppliers to be competitive! A very strange way of conceiving competition, which is not without social consequences: the regulated sales tariff still concerns 68% of individual customers. It is the only tariff offered to consumers who have had payment difficulties. It also serves as a benchmark for all offers.

Differentiation in electricity supply focuses on price

Competition was accompanied by a promise – unfulfilled – of lower prices. Alternative suppliers also emphasized the benefits of stimulating innovation and giving consumers a “choice” of offers.

But what to choose, when the technical product delivered in electrical sockets is the same for all? When you consult the offer comparator provided by the French Energy Ombudsman, the selection criteria boil down to the estimated cost “excluding and with promotion/discount and the percentage of green electricity”.

It is this last criterion that enables suppliers to stand out from the crowd by means other than price. However, green offers are based on a system of certificates of origin that is universally denounced.

The false promise of green offers

Green offers are based on Guarantees of Origin (GO), which are supposed to certify the origin of the electricity consumed. Of course, it’s not a matter of choosing the origin of the electricity delivered to the grid at any given moment, since it’s impossible to trace the source of the electrons. Nevertheless, consumers can expect green offers to encourage investment in renewable production.

However, this is not the case: the development of renewable solar and wind energy is due almost exclusively to another, non-market subsidy mechanism: feed-in tariffs, which guarantee producers the necessary visibility in the form of income over the entire amortisation period of their installations. GOs, which take the form of vouchers distributed to renewable producers under certain conditions (and which can be resold on a market), are an inefficient and obscure subsidy mechanism, despite the promise of transparency regarding the origin of the electricity produced. As the same installation cannot claim both the feed-in tariff and the certificate of origin (as this would be a cumulation of two subsidies), the guarantees of origin go mainly to hydroelectric facilities that have already paid for themselves, anywhere in Europe. As one solar producer pointed out in 2019 69 about a quarter of these guarantees of origin correspond to Norwegian hydroelectric production, and some are even located in Iceland, which is not connected to continental Europe!

The Enercoop cooperative points to a few exceptions, very small installations that do not meet the feed-in tariff allocation criteria and for which these certificates could be of interest, but this remains marginal.

For the most part, then, green offers are a sham, a deception of the consumer. EDF, for example, has no qualms about selling green offers that come from the same production facilities as the electricity sold at the regulated tariff, but which is considered to be 100% grey (and therefore not at all renewable)!

The French Energy Regulatory Commission 64 also highlights services designed to help customers consume more intelligently (by avoiding peak hours). In its June 2021 dossier entitled Electricity and natural gas tariffs, it writes in the introduction that consumers now have access to a wide variety of market offers and cites “weekend offers, super off-peak offers, electric vehicle offers, etc.”. These are nothing more and nothing less than offers that have existed for nearly 40 years for industrial customers (green tariffs 15 and 18). Equivalent, simpler offers (because they were sufficient to meet the need for flexibility) have also long existed for individual customers (off-peak tariffs, EJP, Tempo).

In its ” Plea for a return to monopoly “, the CLCV consumers’ association speaks of “zero innovation”, with a “misleading” presentation of “offers” (particularly green offers), offers which “because of their abstract nature […], their complexity and their lack of obvious attractiveness, are conducive to dubious commercial practices”, before concluding: “Beyond the fact that alternative operators have lacked innovation, they are not producers, and when you are not a producer .. it’s harder to innovate”.

In this context of particularly difficult differentiation, it is understandable that alternative suppliers have fought to obtain the means to propose offers cheaper than the regulated sales tariffs… which they have achieved, not by lowering the prices of their own offers, but by pushing the regulated tariffs upwards and making them dependent on wholesale market prices.

On the other hand, with the recent surge in electricity market prices, consumers who had subscribed to offers indexed to these prices found themselves trapped by soaring electricity bills, without having had the impression of making an informed “choice”.

Read more about the lack of differentiation between alternative suppliers’ offers in our fact sheet on the retail electricity market.

Today, the indexation of electricity prices to wholesale market prices is mandatory for all customers.

The results of opening up the market to business customers were very negative: they clearly expressed their wish to keep a regulated sales tariff (see section 4.3). Since then, their representatives have constantly called for stable prices… the opposite of market prices.

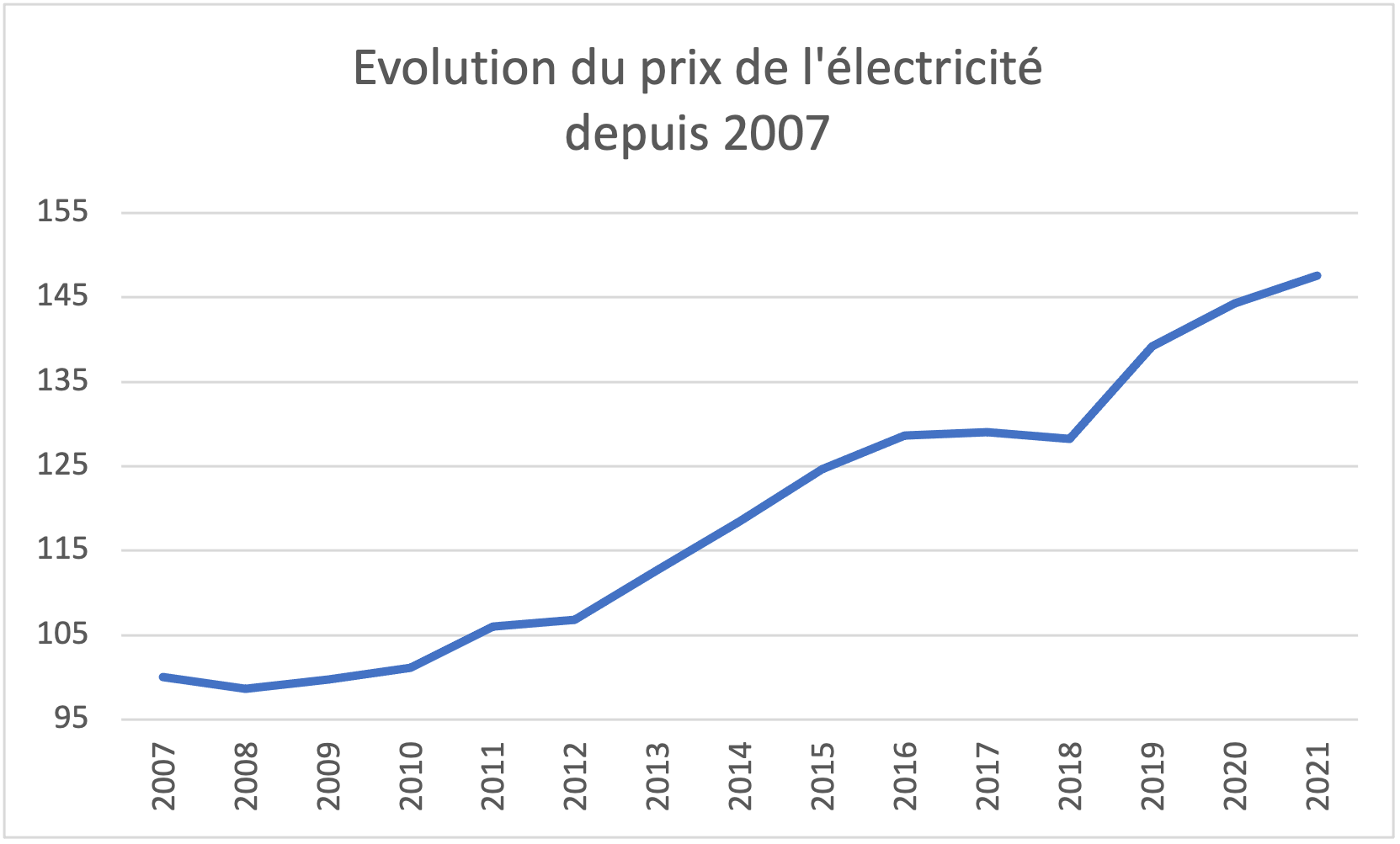

For individual customers, the picture is no better. In France, a study by Insee, supplemented after 2016 by TRV increases published by the Commission de Régulation de l’Energie, shows an increase of almost 50% between 2007 (when the market was opened to private customers) and 2021 in constant euros, i.e. once the effects of inflation have been deducted.

Electricity prices for residential customers since 2007 in constant euros (Base 100 in 2007)

Source 2007-2016: INSEE 2019 note ” Les dépenses des Français en électricité depuis 1960 “; 2017-2021: compilation of deliberations by the Commission de régulation de l’énergie on changes to the regulated sales tariff.

Reading: For an electricity price index set at 100 in 2007, this index would rise to 148 in 2021, i.e. an increase of 48% excluding inflation.

The change in the method of calculating the regulated sales tariff has led to all tariffs and offers to consumers being indexed to wholesale market prices. As a result, bill levels have become much more volatile, and uncontrollable by the public authorities. What’s more, the tariff no longer guarantees to cover production costs (which used to be required by law).

This change in calculation method is one of the main causes of the recent increases.

In 2019, for example, TRVs have risen sharply, not because of an increase in production costs, but because of soaring market prices, as the Commission de régulation de l’énergie wrote in its deliberation justifying these tariff increases 70 . The French competition authority (Autorité de la Concurrence) also emphasized this point, noting that these increases had “nothing to do with the rise in EDF’s production costs”. 71 .

Over the last five years (between August 2016 and August 2021), before the gas price surge of 2021, TRV prices have risen by 18% before tax (25% for the energy portion), while production costs in France have not risen significantly. 72 .

Since the beginning of 2021, soaring global gas prices have led to sharp rises in wholesale electricity prices in Europe, forcing governments to intervene to avoid soaring bills. 73 . In its Communication of October 2021, the European Commission transfers responsibility for resolving the problem to the Member States, authorizing them to take fiscal or aid measures (energy cheques, subsidies, tax reductions, etc.).

Northern European countries follow this line, viewing the surge in wholesale prices as a cyclical episode. Even if the 2021 episode is extreme, the evolution of wholesale prices since their inception proves that they have been highly volatile from the outset (see section 3.1). In 2021, the French government, along with other countries, is defending a reform of the retail market while claiming, against all analysis, that the wholesale market is working properly.

Competition also has non-economic impacts

Challenges to public service, including fair treatment of consumers

The multiplication of market offers, supported by numerous suppliers, is breaking down the equality of treatment between consumers that was guaranteed by a single tariff grid. Individual negotiation is generally unfavorable to the most vulnerable consumers, whose lack of support is also the subject of regular alerts from the Energy Ombudsman.

What’s more, users have to contend with suppliers’ canvassing policies, which are deemed aggressive, offensive and misleading by consumer associations, denounced by the Energy Ombudsman and regularly condemned by the courts. 74 .

Hindering the ecological transition

Furthermore, as we have seen, the market price formation mechanism makes it difficult to finance the massive investments required for the energy transition.

One example among many, recalled by economist Dominique Finon: in Bavaria, storage development projects (hydroelectric pumping stations), essential to the energy transition, were halted due to a drop in the price spread between night and day, following the development of photovoltaics. 75 .

Enormous complexity makes the system fragile and opaque

Today, more and more economists and industry specialists are openly admitting it: nobody understands the ultra-complex mechanisms that have been developed in an attempt to adapt the market to the power system.

Such a “thing” is extremely complex and opaque, reminiscent of derivatives in finance, exposing the system to repeated major crises (as derivatives did in 2008). Under the guise of giving citizens a “choice”, this complexity and opacity effectively prohibit any democratic control over energy policy. 76 .

Threat to energy sovereignty

Finally, the competition imposed by the European Union is placing private multinationals at the heart of a sector that is highly strategic in many respects: for access to an essential commodity, for the economy, for regional planning, for tackling the climate emergency.

In a study for the Institut Français des Relations Internationales (IFRI), the authors denounced the economic, strategic and ecological impact of liberalization back in 2016.