This text has been translated by a machine and has not been reviewed by a human yet. Apologies for any errors or approximations – do not hesitate to send us a message if you spot some!

Introduced in the 2015 Paris Agreement 1the concept of carbon neutrality is defined as achieving a balance between human emissions of greenhouse gases (GHGs) and the removal of CO2 from the atmosphere (via biological or technological absorption and sequestration methods). 2. In other words, to achieve carbon neutrality, we need to be able to absorb and store (sustainably) as much greenhouse gas as we emit.

As we shall see in this fact sheet, this concept only really makes sense on a global scale. However, many companies, local authorities and individuals have set themselves carbon-neutral targets, or even claim to be carbon-neutral. To achieve this, they claim to have “offset” their own emissions, by purchasing carbon credits to finance climate projects.

The aim of this fact sheet is to clarify this debate by giving a precise definition of the terms used, and reviewing the operation and main criticisms of carbon offsetting and credit markets.

Note: carbon neutrality implies being able to count emissions reliably and to define a unit of measurement (the tonne of CO2 equivalent). We therefore advise you to read, before or in addition to this information sheet, the information sheet Counting greenhouse gas emissions, which explains these two points in detail.

What is carbon neutrality?

Definition of carbon neutrality

With the Paris Agreement in 2015, the international community adopted the goal of containing “the rise in global average temperature to well below 2°C above pre-industrial levels” and continuing “action to limit temperature rise to 1.5°C”. What is the link between this objective and that of carbon neutrality?

The rise in global average temperature is largely determined by the accumulation of greenhouse gas (GHG) emissions in the atmosphere, due to human emissions that have been increasing since the start of the industrial revolution. 3.

Stabilizing the global average temperature 4 therefore implies that global GHG emissions, measured in tonnes of CO2 equivalent 5decrease to a level where they are equal to (or less than) the volume of CO2 removed from the atmosphere and sequestered in carbon sinks (seecarbon sinks in section 3.2 below).

The concept of carbon neutrality (or Net Zero Emission) translates this equivalence between emissions and removal from the atmosphere, on a global scale.

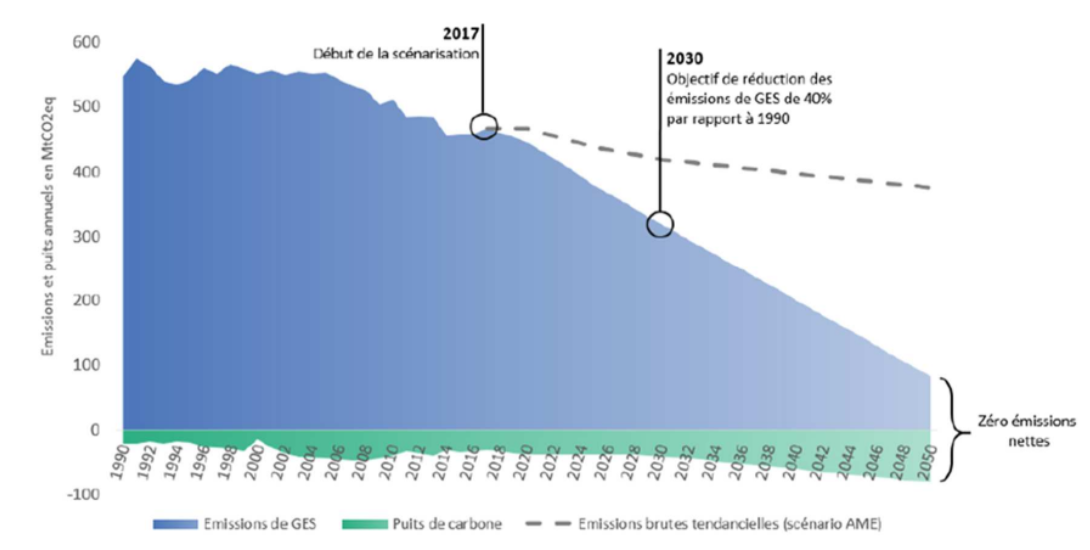

The following image of a carbon-neutral scenario for France clearly illustrates the concept:

Illustration of the carbon neutrality trajectory for France

Source Avis de l’Ademe – Carbon neutrality, 2021

Reading: In 2050, France is expected to emit 80 Mega-tonnes of CO2 equivalent (MtCO2eq). 6 and absorb the same volume in carbon sinks.

Carbon neutrality or GHG neutrality – What are we talking about?

The term carbon neutrality is sometimes used to include all greenhouse gases (in which case it would be more accurate to speak of “GHG neutrality”), and sometimes limited to CO2 alone. It is indeed GHG neutrality that we need to achieve: sequestering CO2 5 removed from the atmosphere must offset emissions of all GHGs combined.

This is indeed what is stated in Article 4 of the Paris Agreement, which sets the objective of “achieving a balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases by the second half of the century”.

The concept of carbon budgeting complements that of carbon neutrality

Achieving carbon neutrality is necessary, but not sufficient to guarantee compliance with the objectives of the Paris Agreement. Indeed, global warming will depend on the cumulative emissions that will take place up to the moment when global carbon neutrality is achieved. The sooner carbon neutrality is achieved, the lower the level of global warming.

It is this dimension that the carbon budget makes it possible to transcribe: it designates the cumulative quantity of CO2 we can still emit to stay below a certain level of warming compared with the pre-industrial period (generally that corresponding to international targets, i.e. +2°C or +1.5°C). While the carbon budget concept is the most developed at scientific level, it obviously needs to be supplemented by estimates of emissions of other GHGs (methane budget, N2O).

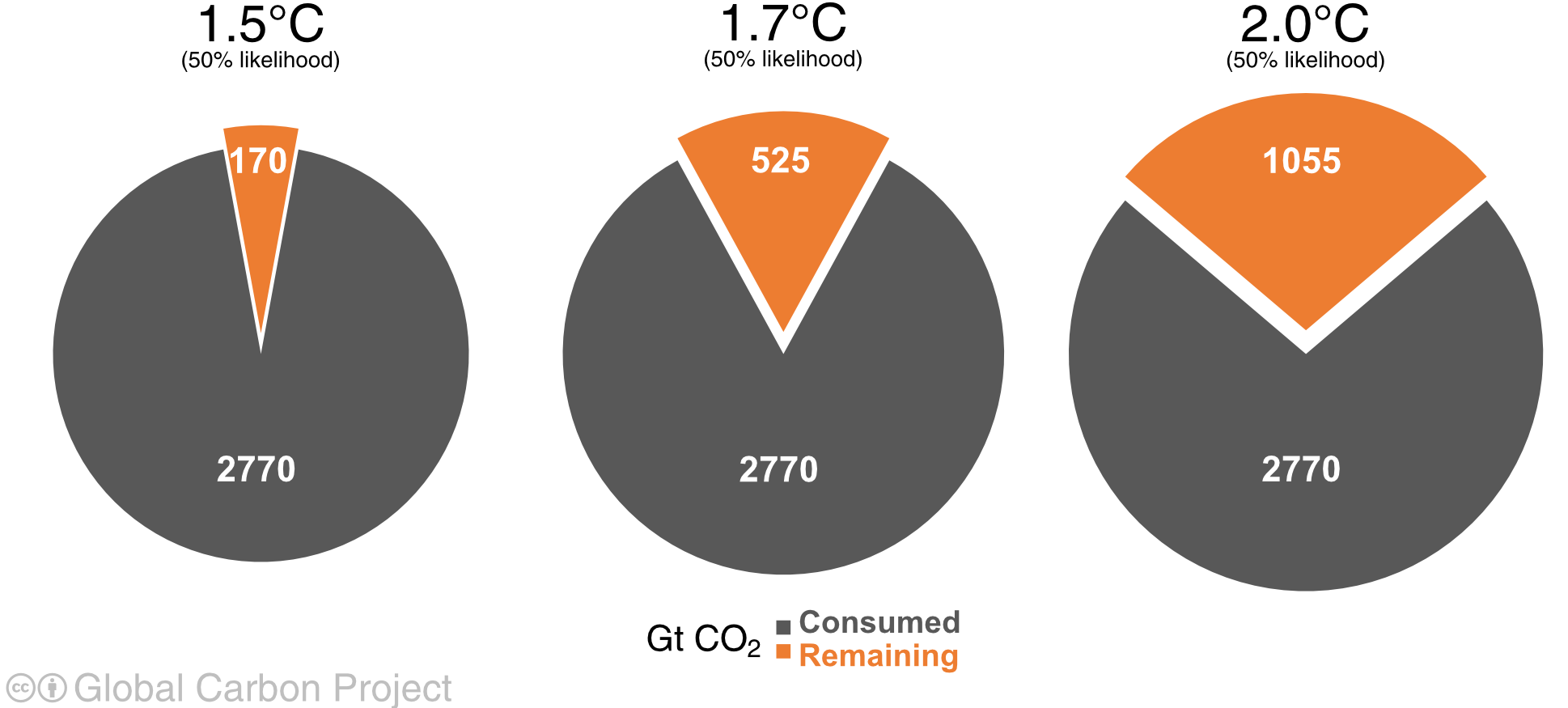

What is the global carbon budget at the end of 2024?

According to the Global Carbon Budget 2025 report 8 meeting the 2°C objective with a probability of 50% implies, a remaining carbon budget of 1055 billion tonnes of CO2, from January 2025. This is equivalent to 26 years of current emissions (around 40 GtCO2 per year over the last decade).

Source Figures from the Global Carbon Budget 2025

Reading: historical cumulative human emissions amounted to around 2770 Gt CO2 at the end of 2024. From January 2025, the maximum carbon budget to limit global warming to 2°C (with a probability of 50%) is 1055 Gt CO2.

Carbon neutrality only makes sense on a global scale

In its opinion on carbon neutrality (2021), Ademe asserts that carbon neutrality is a notion that only makes sense on a planetary scale or, to a lesser extent, on a national scale. There are two reasons for this stance.

The issue of program allocation is complex

The first reason is methodological: it is difficult to attribute emissions to a particular player in an indisputable manner.

In fact, all players share responsibility for the indirect emissions linked to their activity (those linked to the manufacture of goods and services consumed or the use of goods and services sold).

For example, a carmaker shares responsibility with its customers: by manufacturing cars that are heavier or lighter, with more or less emission-intensive technologies, it partly determines the emissions linked to vehicle use. Of course, these emissions also depend on the number of kilometers driven and the driving habits of customers. In addition, the presence and quality of infrastructure, as well as the existence of regulations, which depend on public authorities, also influence emissions linked to automobile transport.

This makes it impossible to add up the efforts of the various players without counting certain emissions several times over. This is known as the risk of double counting. Similarly, if a player (the carmaker, for example) finances an emission-reduction action outside its value chain (reforestation of an area, for example), its responsibility is shared here too.

The second reason is as much methodological as ethical. Not all players have the same capacity to be carbon neutral. Collective neutrality can be achieved in many ways. It may be more efficient, and sometimes fairer, for some players to be “more than neutral”, while others may be “less than neutral”, depending on their individual possibilities for balancing emissions and sequestration.

For example, if the objective of carbon neutrality is not pursued at national level, a territory covered by a large forest area could benefit from this sequestration well without having to pursue an ambitious ecological policy, whereas a territory without a forest area would be forced to make much greater efforts to reduce emissions.

A fair contribution to collective neutrality therefore implies that some territories should aim for higher ambitions – such as becoming net negative in the case of rural territories with a high proportion of carbon sinks; and others, for lower ambitions in the case, for example, of urban or highly industrialized territories, which will always have no choice but to emit more than they sequester.

This discussion also concerns companies, some of which are much more carbon-intensive than others, even though the goods and services they produce are essential (as in agriculture, for example). More generally, while all activities should aim for carbon neutrality, some cannot, or only with great difficulty.

The concept of carbon neutrality cannot therefore be applied strictly to a single organization or territory, which are all contributing to the trajectory towards global carbon neutrality.

However, carbon neutrality can also be applied at national level

While, in theory, the two arguments above are equally valid for States, the United Nations Convention on Climate Change (1992) has, from the outset, removed the methodological obstacle by establishing the responsibility of each State for its emissions and absorptions linked to its territory. 9.

Following the signing of the Paris Agreement, many countries made commitments to achieve carbon neutrality by a given date, whether through legislation, strategic plans or simple declarations. The Net Zero Track er Observatory makes it possible to monitor the progress of these commitments.

On a European scale: the Green Deal

In 2019, with the GreenDeal for Europe, the European Union launched a roadmap to make Europe climate neutral by 2050.

This objective became legally binding in 2021 with the adoption by the EU Council of the European Climate Neutrality Regulation.

It also enshrines the intermediate “Fit for 55” objective of reducing the European Union’s net GHG emissions by at least 55% by 2030, compared with 1990 levels.

In France: the National Low Carbon Strategy

National Low Carbon Strategy (SNBC ) 10 is France’s roadmap in the fight against climate change. It describes the path to be followed to achieve long-term national targets for reducing greenhouse gas emissions and increasing carbon sinks. It defines, for each 5-year period, “carbon budgets” specifying ceilings on greenhouse gas emissions that must not be exceeded, expressed as an annual average. These include all GHGs (and therefore not just CO2, unlike the global carbon budget mentioned in section1.2) and are broken down by sector: transport, agriculture, industry, buildings, energy production and conversion, waste, carbon sinks (i.e. forests and land use change).

The SNCB was first adopted in 2015 with a target of dividing France’s GHG emissions by 4 by 2050 compared with 1990.

In 2020, the SNBC 2 reflected France’s increased climate ambitions: the aim is now to achieve carbon neutrality by 2050.

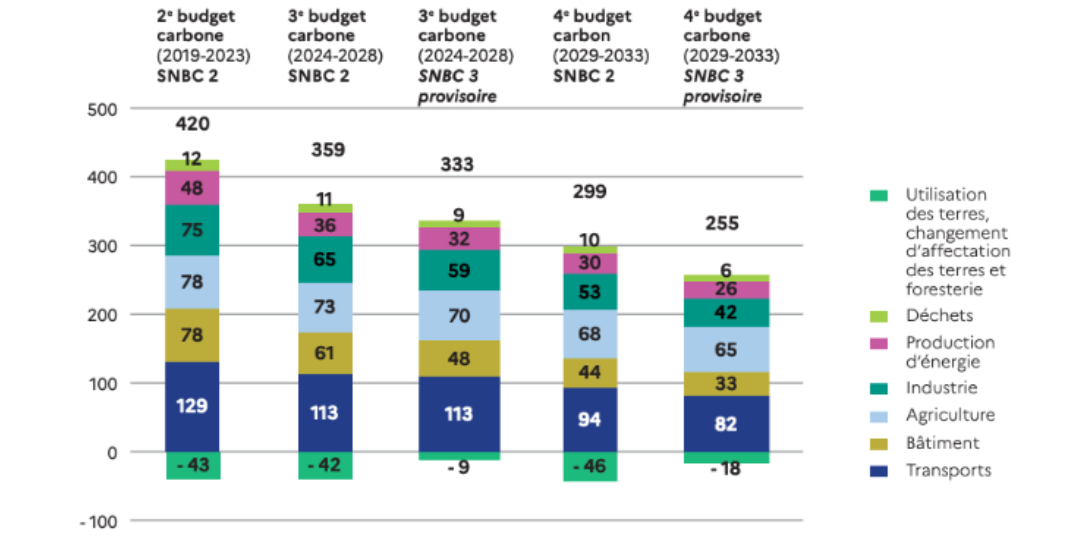

By the end of 2024, SNBC 3 was under consultation. The revision timetable was delayed by a problem of “looping”, i.e. overall consistency. On the one hand, the 2030 ambition had to be revised upwards to be consistent with the European intermediate target. Secondly, carbon sinks had been overestimated in SNBC 2 in relation to their actual absorption capacity. In SNBC 3, it was therefore necessary to revise them downwards, which implies additional efforts for other sectors. This can be seen in the following graph.

Comparison of carbon budgets for SNBC 2 and SNBC 3

Source SNBC 3 press kit (4/11/24). See also the consultation documents for more details.

Reading: The annual GHG emissions target for the 3rd carbon budget (2024-2028) is 359 MteqCO2 5 in SNBC 2 and 333 MteqCO2 in SNBC 3. Carbon sinks go from an absorption of 42 MteqCO2 in SNBC 2 to 9 in SNBC 3.

Note: unlike the global carbon budget mentioned in section 1.1, which only concerns CO2, the carbon budgets used in the SNBC include all GHGs.

The first carbon budget under the SNBC (2015-2018) was exceeded by 61 Mt CO2eq 5 or 3%. In February 2021, in “L’Affaire du Siècle”, this overshoot was sanctioned by the courts, which recognized the existence of “ecological damage” and the State’s obligation to catch up. 13.

In its 2024 annual report, the Haut Conseil pour le Climat wrote: “The 2nd carbon budget of the SNBC 2 for net emissions (including the LULUCF sector” 14“) is on track to be exceeded, due to the low level of carbon sinks second carbon budget (2019 – 2023).”

What are the levers of carbon neutrality?

Carbon neutrality is based on a fairly intuitive equation: the aim is to emit, in tonnes CO2eq 15 only what we are capable of removing from the atmosphere, so that the level of GHG accumulation in the atmosphere no longer increases.

As you can see, we need to act on two levers:

- reduce greenhouse gas emissions;

- secondly, to remove CO2 from the atmosphere and sequester it in anthropogenic carbon sinks.

First lever: reducing greenhouse gas emissions

As highlighted in section 1.1, although we speak of “carbon neutrality”, this actually concerns all greenhouse gases: methane (CH4), carbon dioxide (CO2), nitrous oxide (N2O) and halocarbons… While GHGs are the result of natural chemical and physical processes (with the exception of halocarbons), they are also (and above all) the result of human activities, and concern all economic sectors.

Worldwide direct and indirect greenhouse gas emissions by end-use sector in 2019

In 2019, anthropogenic greenhouse gas emissions totaled 59 GtCo2eq, broken down as follows.

MISSING DATAVIZ: emissions-directes-et-indirectes-de-gaz-a-effet-de-serre-mondiales-par-secteur-final-dutilisation-en-2019Source IPCC Sixth Assessment Report (2022) – Working Group 3 – Chapter 2 (figure 2.12).

In this graph, indirect emissions (i.e. those linked to electricity and heat production) are allocated to the final consumption sectors (e.g. buildings).

The Energy sector therefore only includes other emissions linked to energy production (e.g. fugitive emissions from fossil industries, oil refining, etc.).

LULUCF = Land Use, Land Use Change and Forestry.

For example, methane (CH4) emissions are linked to ruminant breeding (mainly cattle and sheep), certain agricultural crops (notably rice), waste dumps, and leaks from coal, oil and gas extraction.

Human activities are also increasing emissions of nitrous oxide (N2O), notably through the use of nitrogen fertilizers in agriculture, wastewater treatment, fossil fuel combustion and certain chemical processes.

Carbon dioxide (CO2), the main GHG emitted by mankind, is notably linked to the combustion of fossil fuels (oil, gas, coal), to the chemical reactions underlying certain industries (cement production) and to deforestation.

The first lever is therefore to take action in all sectors to reduce as far as possible the GHG emissions caused by human activities. Each sector of activity and each player must therefore (by taking into account its entire production – consumption – end-of-life chain) establish specific actions to decarbonize.

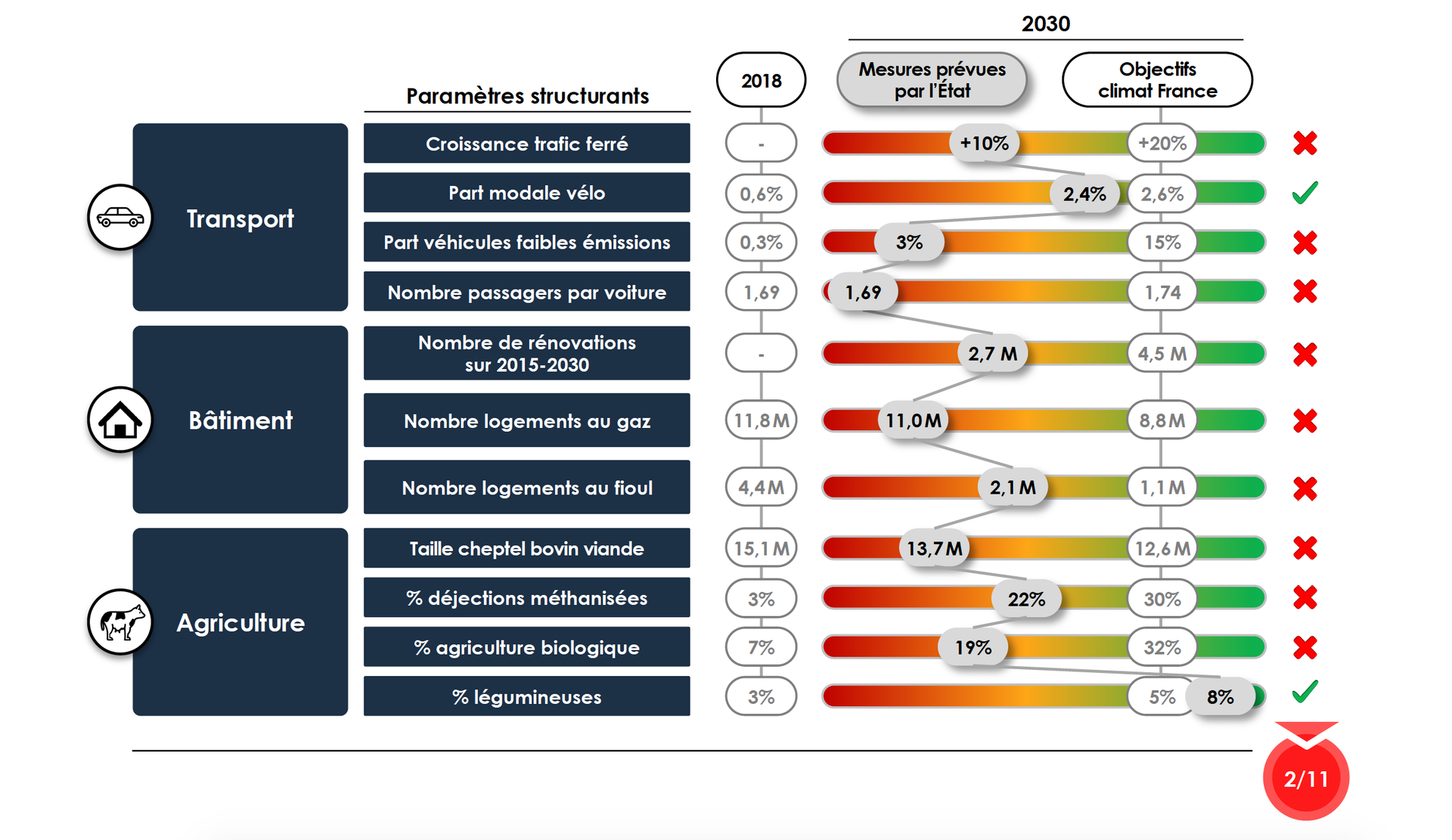

In 2021, Carbone 4 16 has identified eleven structuring parameters for reducing greenhouse gas emissions in three key sectors (passenger transport, housing, agriculture). The measures identified include, for example, energy renovation in the building sector, and reducing the use of oil and gas heating.

Source L’État français se donne-t-il les moyens de son ambition climat, Carbone 4, 2021.

Reading: Analysis of the measures implemented by the French government shows that they were insufficient in 2021 to achieve the reduction targets set by the SNBC.

Second lever: removing carbon from the atmosphere and sequestering it in anthropogenic carbon sinks

A “carbon sink” is a reservoir (other than the atmosphere) in which carbon is stored for a long time. A distinction is made between natural and anthropogenic carbon sinks.

Given the current state of knowledge and technology, CO2 is the only greenhouse gas that can be removed from the atmosphere by human action. The carbon that makes up this gas is then stored in anthropogenic carbon sinks, either in organic form (in biomass in particular) or in its gaseous form (in the case of technological sinks).

The two types of natural carbon sink

The oceans are the most important reservoir: carbon is stored there in inorganic form (dissolved in water or in particulate form, notably in the shells of marine organisms), and in organic form in living organisms.

Land areas not managed by humans (boreal and tropical forests, inland waters and estuaries): carbon is stored in organic matter and soils.

Carbon is constantly being exchanged between the ocean, unmanaged land and the atmosphere. 17. They have increased due to human CO2 emissions, of which around half are absorbed and stored each year in natural carbon sinks 18. The rest accumulates in the atmosphere: without these natural sinks, global warming would be much more pronounced.

Anthropogenic carbon sinks

For various reasons, the concept of carbon neutrality does not refer to natural carbon sinks. 19 but to anthropogenic sinks, which are linked to human actions aimed at removing carbon from the atmosphere. These can be grouped into two categories:

–Anthropogenic biological sinks refer to the reservoir of biomass managed by humans (forests, grasslands, farmland, nature reserves, etc.).

In GHG emission inventories, it is the “land use, land-use change and forestry” (LULUCF) sector that reflects the annual evolution of this well. Unfortunately, today it is a source of emissions on a global scale, due to deforestation, artificialization and intensive agricultural practices. 20.

Reversing the trend would require putting an end to these practices and developing reforestation and afforestation policies. 21and wetland restoration, as well as farming practices that increase soil carbon storage, such as the use of biochar.

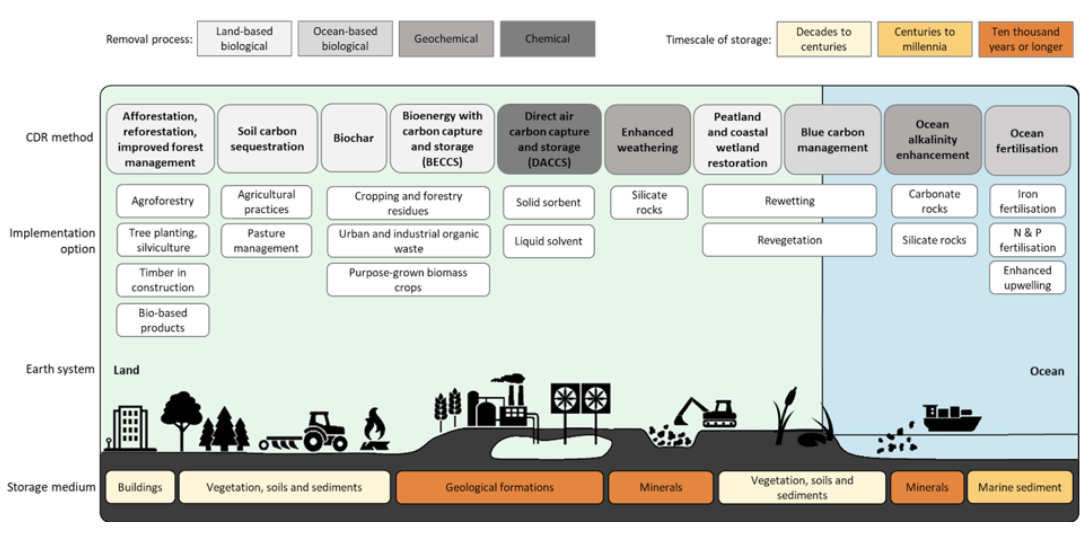

– Anthropogenic technological sinks refer to practices involving technology.

The two best-known techniques involve capturing CO2 from the atmosphere (either directly via machines, or indirectly by burning biomass and capturing the emissions released during combustion). 22) and then injecting it into geological reservoirs.

Although they are attracting a great deal of attention in the public debate (as well as in terms of research and funding), these technologies are still emerging and far from the necessary scale-up.

The potential of direct airborne capture (DACCS) was analyzed by an MIT team in 2024 23. At this stage, it is very low for energy and cost reasons. In fact, this type of project captures very little carbon.

Given the importance of the stakes involved in climate change, it’s unwise to count on the DAC to be the hero who comes to our rescue.

Classification of techniques for removing carbon from the atmosphere

Source Climate Change 2022: Impacts, Adaptation and Vulnerability. Contribution of WG II to the 6th IPCC report – Cross-Chapter Box 8, Figure 1

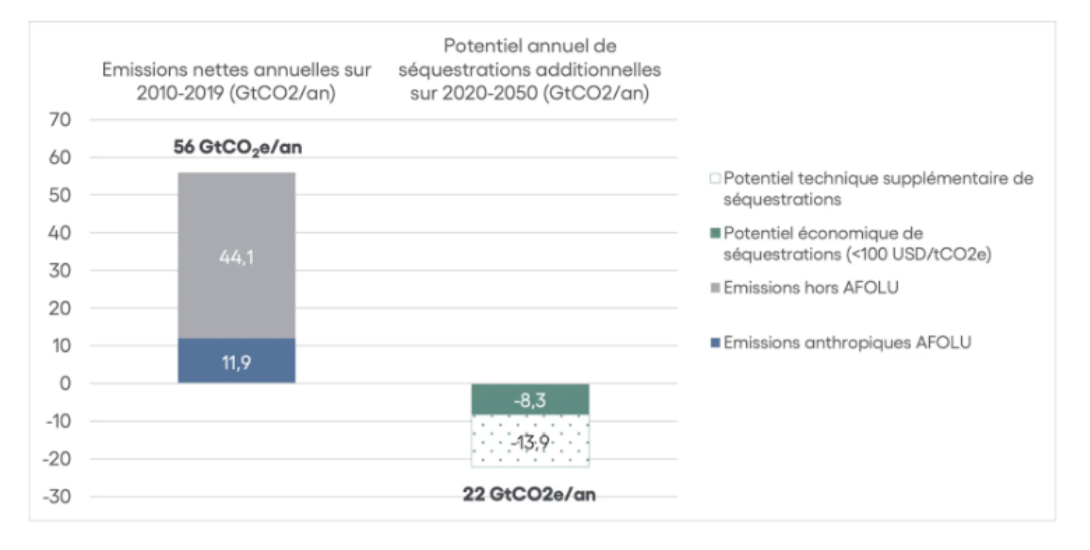

It is important to note that the potential for carbon sequestration in anthropogenic sinks is limited and largely insufficient to achieve carbon neutrality. As shown in the graph below, in the early 2020s, it was optimistically projected at 22 giga tonnes CO2 equivalent per year over the period 2020-2050. This potential is therefore largely insufficient to offset global GHG emissions, which amounted to 56 GtCO2eq. 5 over the 2010-2019 period 25. Emissions reduction is therefore a priority.

Average annual net greenhouse gas emissions over the period 2010-2019, and annual potential for additional sequestration over the period 2020-2050, in GtCO2eq/year.

Source Puits de carbone : de quoi parle et quel potentiel au niveau planétaire, Carbone 4, 2024. Note: AFOLU stands for Agriculture, Forestry, and Other Land-Use.

The authors of the article point out that “the effective mobilization of this potential faces major challenges in practice, and is far from a foregone conclusion: technical and organizational challenges linked to changes in practices; competition for land use in contexts of demographic and/or economic growth; access to appropriate and sufficient financing; impact of climate change on ecosystems.”

Find out more

On removing carbon from the atmosphere

- Carbon sinks: what are we talking about and what is their global potential?, Carbone 4 (06/12/24)

- A guide to techniques for removing CO2 from the atmosphere, Carbon Market watch (2024)

- Carbon capture and storage: scam or climate solution? Emmanuel Pont on Blog Pote (13/11/24)

- The NEGEM European research project on negative emissions technologies and practices

How can companies contribute to carbon neutrality?

While governments have a major role to play (investment, regulation, incentives), businesses are key players if we are to achieve GHG neutrality.

To provide a framework for practices in this area and avoid greenwashing, guidelines have been developed, whether for counting an organization’s GHG emissions or implementing decarbonization strategies.

Frameworks with different objectives

The GHG Protocol proposes a standard, first published in 2001, widely used worldwide to measure the greenhouse gas emissions of public and private players. In France, the tool used is the Bilan GES (or Bilan Carbone), developed by Ademe.

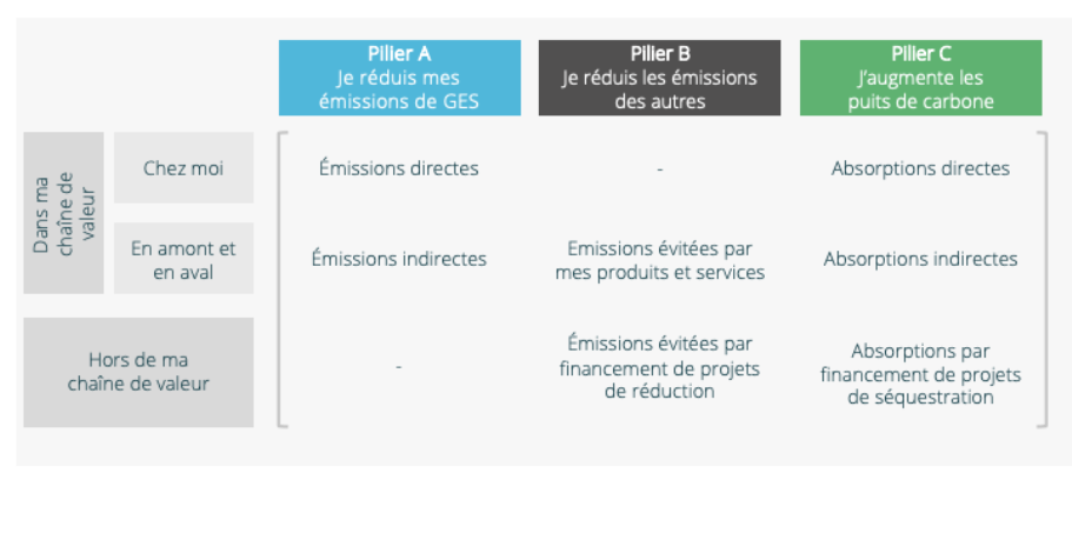

The Net Zero Initiative (NZI) complements the GHG protocol or Bilan Carbone. It sets out a typology of the main types of action that an organization can take to contribute to carbon neutrality, in addition to reducing its own GHG emissions. One of the aims of this initiative is to set limits on the use of carbon neutrality terminology by companies.

The Science-based Target Initiative (SBTi) is a global reference framework to help companies determine decarbonization trajectories compatible with the Paris Agreement. The first edition was published in 2015, and is broken down by major economic sector.

Initiated in 2018 by Carbone 4 16 ADEME, the French Ministry of Ecological Transition, and around twenty companies, the NZI’s work has highlighted three main types of actions, simultaneous but quite distinct, that a company can take to contribute to planetary carbon neutrality:

- Reduce your own emissions as much as possible.

- Help other players reduce their emissions.

- Contribute to the net creation of carbon sinks, both within and outside its value chain.

The three pillars of the Net Zero Initiative standard

Source Net Zero Initiative, A framework for collective carbon neutrality, 2020

Reducing company emissions is top priority

To reduce its emissions, a company must first measure them. To do this, it must draw up a carbon footprint, i.e. a quantified inventory of GHG emissions over the course of a year. This diagnostic tool measures a company’s (or a local authority’s) dependence on fossil fuels and, more generally, the GHG emissions it generates.

It also helps to identify where the company has room for maneuver and where it needs to focus its efforts.

Avoided emissions

A company can contribute to Pillar B of the NZI in two main ways: via the goods and services it sells, and/or by financing emission reduction projects outside its value chain.

We speak of “avoided emissions” thanks to a company, when the product or service it sells enables its customer to reduce the emissions it would have generated without using this product or service. For example, the sale of thermal insulation for a home or piece of equipment (such as a hot water tank) “avoids” emissions for the purchaser, by reducing (all other things being equal) the energy consumption of this equipment or home.

A company can also contribute to Pillar B by financing emission reduction projects outside its value chain, for example by purchasing carbon credits from building renovation projects(see section 4 on carbon markets).

The level of avoided emissions is then equal to the difference between the level of GHG emissions observed following the implementation of a project/product/service (for example, the use of insulation), and the level of GHG emissions that would have been observed in the absence of this project/product/service (if the insulation had not been installed). An avoided emission therefore depends on a so-called “reference scenario” (or counterfactual scenario), which reflects the most likely situation that would have occurred in the absence of the project.

It is important to note that the emissions avoided, although expressed in tonnes of CO2 equivalent 5equivalent, are not of the same nature as absolute GHG reductions under Pillar A. Indeed, their calculation involves a difference between a virtual situation (the reference scenario) and a real situation (actual emissions); whereas emissions reductions are a difference between two real situations.

Removing carbon from the atmosphere and sequestering it in anthropogenic carbon sinks

Pillar C of the NZI breaks down into three categories:

- direct carbon sinks owned by the company (e.g. afforestation of land owned by the company);

- indirect carbon sinks, upstream or downstream of its value chain (for example, the company’s collaboration with the farmers who supply it, to encourage them to develop carbon-storing farming practices);

- carbon sinks outside its value chain, by financing reforestation and afforestation projects, etc.

In the report Foundations for net-zero target-setting in the corporate sector published in 2020, the Science-based Target Initiative (SBTi) estimates that the “right level of sinks” to be achieved in 2050 should be the equivalent of the company’s residual emissions in 2050, after having reduced its emissions along a trajectory compatible with a warming of 1.5°C. 28.

The method developed by NZI suggests that companies ensure that, each year, their ratio of Pillar C (actions to develop carbon sinks) to Pillar A (emissions reductions) is equal to the ratio of absorptions to emissions associated with a global reference scenario. 29.

Let’s take the example of a scenario compatible with 1.5°C 28 scenario. Each year, it is possible to calculate a ratio of absorptions to emissions compatible with this objective. This ratio is, for example, 0.2 at the end of the 2020 decade. 31. This means that a company is committed to ensuring that its own C pillar / A pillar ratio follows the same trend. In concrete terms, this means that the company aims to develop sinks equivalent to 20% of their emissions by 2030.

Carbon offsetting is part of the broader carbon market framework

As mentioned in section 3.3, a company -and more generally any economic player- can contribute to carbon neutrality by financing a project to reduce GHG emissions or sequester carbon, outside its value chain. This investment in projects run by others is most often referred to as “carbon offsetting”. In this section, we present the market mechanisms on which “carbon offsetting” is based.

It should be noted from the outset that this name is problematic, as it suggests that all a company needs to do to become “carbon neutral” is to “offset” the emissions it has failed (or not sought) to reduce. Worse still, it would be enough for all companies to be “carbon neutral” in this way to achieve global neutrality.

This is obviously not possible, because if companies simply “offset” their emissions by financing reduction or sequestration actions by others, who will reduce the emissions for which they are directly responsible?

Carbon markets: understanding the difference between the GHG emissions trading market and the carbon credit market

Although the idea of using market mechanisms to reduce pollution first appeared in the 1960s 32it was with the Kyoto Protocol (1997), the first binding international agreement on climate, that it really took off. In this agreement, the developed countries (known as Annex B countries) 33) undertook to collectively reduce their emissions by 5% from 1990 levels over the period 2008-2012. This general target was then broken down by country.

The Kyoto Protocol provided for two types of market mechanisms to help countries meet their targets. These two main categories have been maintained to this day.

Emissions trading schemes

These are regulatory markets designed to reduce the GHG emissions of economic players in a given sector (or territory). The market’s organizing authority sets an overall GHG emissions ceiling for all players involved in the market for a given period. This overall target is then broken down by player: each participant receives (free of charge or via an auction system) the allowances corresponding to the emissions it is entitled to emit. If, over the period in question, its emissions exceed its allowances, it must buy allowances on the market from other players, or pay a fine. The overall cap (and its breakdown by player) is supposed to decrease steadily in order to achieve the emission reduction targets set for the sector or territory concerned.

The Kyoto Protocol called for the creation of a global quota market, but this never came into being. However, a number of regional carbon markets now exist: in 2005, the European Union created theEuropean Union Emissions Trading Scheme (EU ETS), which concerns companies in energy-intensive sectors; the Regional Greenhouse Gas Initiative has been in existence in the northeastern United States since 2009, and Quebec has had acap-and-trade system since 2013.

Carbon credit markets

Their aim is to recognize the actions taken by project developers to reduce the emissions of other economic players or to sequester carbon.

A certifying authority allocates credits to project developers based on the estimated impact of their action. These credits can then be sold on carbon credit markets to raise financing for the climate projects they are developing. Once on the market, the credits can be traded repeatedly until an end-buyer decides to use them, as part of legal obligations or communication objectives (e.g., a company’s “carbon neutrality” display). The credit is then “withdrawn” from the market and can no longer be traded.

Carbon credit markets are most often established on a voluntary basis(see section 4.2), but some have a regulatory basis.

This is the case for the first of them:theClean Development Mechanism (CDM) under the Kyoto Protocol. It enabled companies from Annex B countries

33 countries to implement and/or co-finance GHG emission reduction projects in developing countries. In return, they received carbon credits 35 the amount of which corresponded to the GHG emissions avoided thanks to the implementation of the project, compared with a baseline scenario without the project. Companies could sell these carbon credits, and governments could count them towards their Kyoto Protocol reduction targets. After 2020, registration of CDM projects has been suspended pending implementation of Article 6.4 of the Paris Agreement.

Article 6 of the Paris Agreement creates two new international carbon markets

Interstate carbon trading (article 6.2)

Countries that have achieved emission reductions in excess of those set in theirNationally Determined Contributions (NDCs) 36 generate carbon credits known as ITMOs(Internationally Transferred Mitigation Outcomes). They can then sell them to countries that have failed to meet their targets. In May 2023, for example, Switzerland submitted its first “initial report on art.6.2”, in which it mentions the purchase of ITMOs from Ghana, Thailand and Vanuatu.

This market is a kind of quota market, with one major difference: emissions caps are not set by an independent authority, but by the States themselves. This raises the question of efficiency, as the overall cap is far too high: by the end of 2024, the sum of all the GHG emission reduction targets set by the States in the NDCs would lead to global warming in excess of +3°C. 37.

The Paris Agreement Credit Mechanism (Art 6.4)

After 10 years of negotiations 38the modalities for implementing Article 6.4 culminated at the Baku climate COP (2024), where the new rules were adopted. Once the market is operational, developers of a GHG emissions reduction or carbon sequestration project will have to apply for registration with theArticle 6.4 Supervisory Body, set up by the UN. The project must then be approved by both the country in which it is implemented and the monitoring body before it can begin issuing UN-recognized carbon credits. These credits can then be purchased by countries, companies or even individuals. It should be noted that projects registered under the Kyoto CDM can be transferred to the Article 6.4 mechanism. 39 .

Source To find out more about the market mechanisms set up under Article 6 of the Paris Agreement, see the CarbonMarket Watch FAQ and the article Tout comprendre (enfin) à l’article 6 de l’accord de Paris sur les marchés carbone adopté après neuf ans de négociations, AEF info (10/03/25).

The difference between quota markets and credit markets lies in the actors responsible for emissions and in the objective of the market.

In both cases, participating players exchange financial instruments representing greenhouse gas emissions (generally expressed in tonnes of CO2 equivalent).

Carbon quotas represent the maximum emissions that players in the sector concerned by the market are allowed to emit. The aim is to reduce them globally by gradually lowering the caps.

In the case of carbon credit markets, the aim is essentially to provide financing for emission reduction (or carbon sequestration) projects by individuals, local authorities or businesses – and for buyers to be able to communicate their climate contribution.

As already noted, the problem arises when carbon credits are used to “offset” a player’s own emissions, in place of its own reduction actions. The question of the interface and communication between the two types of market is therefore an important one.

Focus on voluntary carbon credit markets

As noted above, there are various types of carbon market. Here, we will focus on voluntary credit markets.

What is a voluntary carbon credit market?

Voluntary markets developed in parallel with the Kyoto Protocol mechanisms, sometimes referred to as “compliance markets”, because they were part of the process of achieving regulatory targets.

In voluntary markets, players purchasing carbon credits do not do so to meet a legal requirement. They therefore concern players who are not subject to any constraints on their GHG emissions (private individuals, local authorities, etc.), or those who wish to go beyond their obligations and demonstrate their ecological commitment.

However, according to the NGO Carbon Market Watch, the line between voluntary and compliance markets is becoming increasingly blurred as carbon credit markets develop. Taking the aviation sector as an example, the NGO points out that, for a given carbon credit, the credit will be considered part of the compliance market if it is purchased to meet the obligation set under the UN’s “Carbon Offsetting and Reduction Scheme for International Aviation” (CORSIA). The same credit would be considered “voluntary” if purchased for other purposes (for example, as part of a public relations campaign). Yet it would be the same credit, from the same project, purchased by the same airline. This example shows that the distinction is rather artificial and not particularly useful or informative.

A growing market dominated by a handful of players

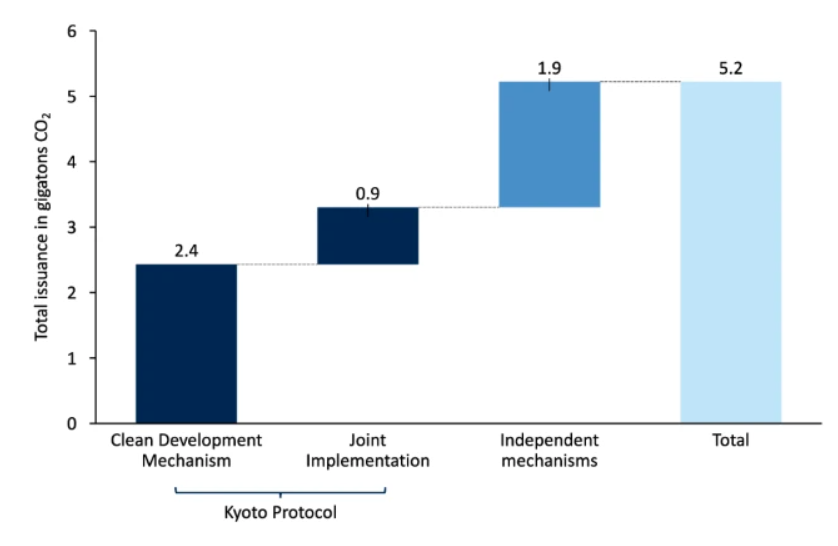

Since the launch of carbon credit markets following the Kyoto Protocol, over 5 billion tCO2e of carbon credits have been issued, including 1.9 billion for voluntary markets.

Cumulative carbon credit emissions from origin to end 2023

Source Benedict S. Probst, Malte Toetzke, Andreas Kontoleon et al. Probst, Malte Toetzke, Andreas Kontoleon et al. Systematic assessment of the achieved emission reductions of carbon crediting projects, Nature Communications, 2024 (Figure 1a)

Reading

Carbon credit emissions from Kyoto Protocol mechanisms (Clean Development Mechanism and Joint Implementation) amounted to 3.3 GtCO2e.

Carbon credit emissions from the 4 main voluntary market standards (American Carbon Registry _ ACR, Climate Action Reserve _CAR, Gold Standard _GS) and Verra) amounted to 1.9 GTCO2e.

Voluntary carbon markets have grown significantly in recent years: over 286 million credits (expressed in tonnes of CO2eq 5) were generated in 2023, compared with around 5 million in 2017 41. According to the NGO Climate Crisis Advisory Group 42 voluntary markets could generate around 2 billion euros in financing for climate projects.

In order to sell carbon credits, a project developer must followthe standard of the market on which he wishes to register his project. While procedures may vary from one standard to another, on the whole, they all follow the same eight-step process, from project design to carbon credit issuance and trading. 43. The role of the organizations that develop carbon market standards is to validate that the proposed project meets the standard’s norms, register it and issue the carbon credit, after verification by an independent auditor that the project has indeed achieved the expected objectives. Credits issued in this way are recorded in the developer’s account in the relevant standard’s register.

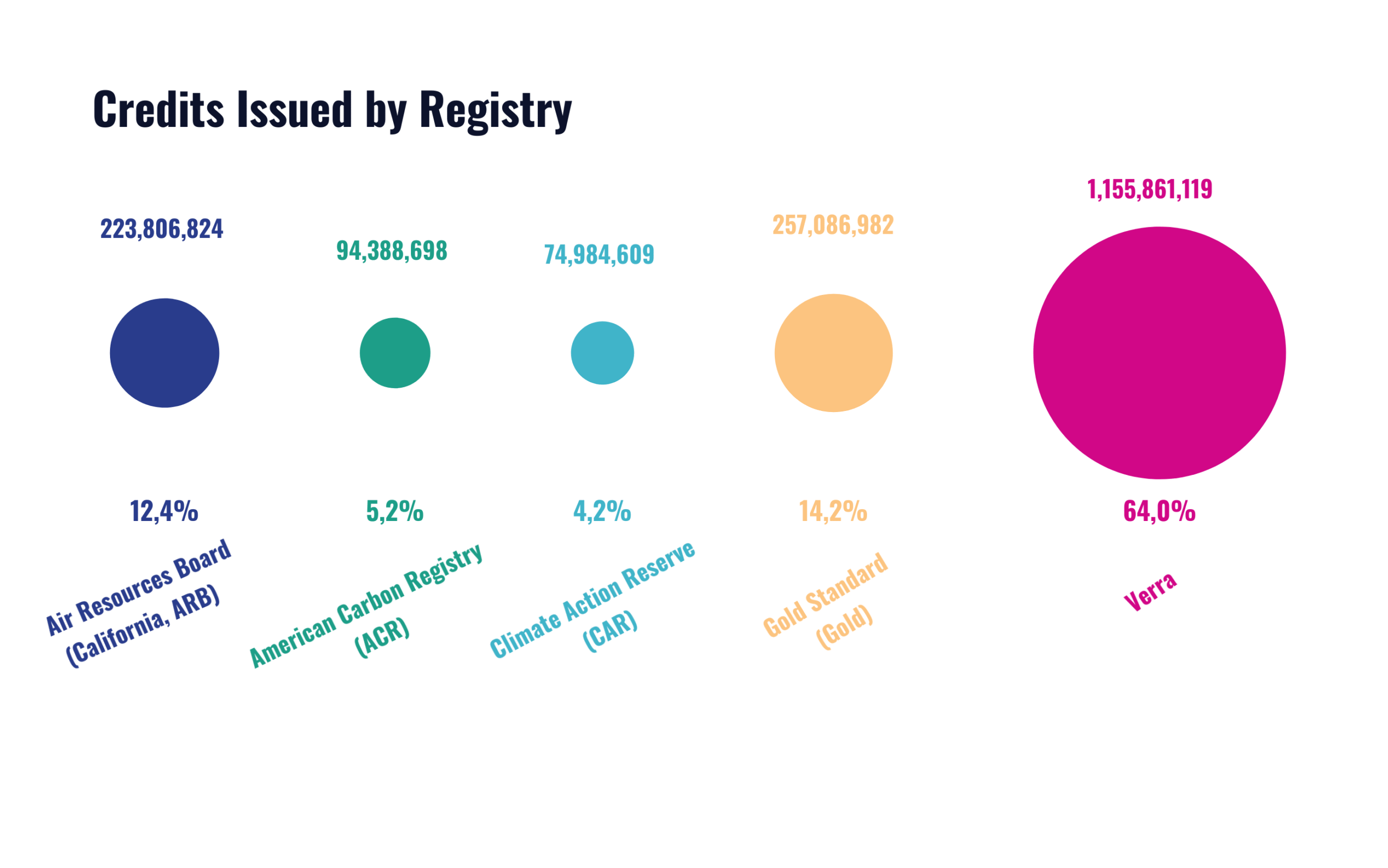

As can be seen from the following graph, the market is concentrated around a few players. The first of these, Verra, had generated around 64% of the carbon credits issued since the start of the voluntary markets by May 2023.

Carbon credits issued by standards developers from inception to May 2023

Source Carbon Markets 101 – The ultimate guide to market-based climate mechanisms, Carbon Market Watch, 2024

REDD+ at the heart of voluntary carbon markets

Set up as part of the United Nations Framework Convention on Climate Change, REDD+(Reducing Emissions from Deforestation and forest Degradation) was initially a program designed to provide results-based funding for projects to combat deforestation. The aim was to enable developing countries to receive funds to protect their primary forests. It did not allow for the creation of carbon credits.

The program has, however, been hijacked from its original spirit by certain private standards. One example is the Voluntary Carbon Standard (VCS), managed by Verra, which has developed methodologies for issuing carbon credits for REDD+ projects. By mid-May 2023, Verra had certified 97 REDD+ projects, generating 445 million credits.

This development has been widely criticized for the exaggerated quantities of credits that the projects generate, and above all for their highly questionable climate impact: REDD+ projects approved by the United Nations are simply examined by experts appointed by the Framework Convention; there is nothing to prevent a country from massively exaggerating the impact of its programs, and nothing to guarantee the permanence of the measures taken. Find out more in section 5.1).

Source Exposing the methodological failures of REDD+ forestry projects

Find out more

- Carbon Market watch educational FAQs

- Carbon Markets 101 – The ultimate guide to market-based climate mechanisms, Carbon Market Watch, 2024

- Carbon prices live

- Database of offset projects (and related credits) registered on the first four voluntary carbon credit market registries, Berkeley Carbon Trading Project

- Carbon offsets: episode of Last Week Tonight (John Oliver)

Do “carbon offset” mechanisms really contribute to carbon neutrality?

While “carbon offsetting” appears to be a useful mechanism for financing climate projects, it is deeply problematic for two main reasons.

The first is the difficulty of guaranteeing the added value and actual impact on the climate of the projects underlying offsetting. As we shall see, many studies question the real impact of offsetting on the climate. Certain essential criteria, such as the additionality and permanence of climate gains, are not, in fact, often respected.

The second criticism concerns the vision of decarbonization induced by the semantic field of offsetting. It’s a vision in which reducing emissions at home and at others is equivalent. This encourages, or even enables, major emitters to shirk their responsibilities (i.e., not to decarbonize their activity, and to continue business as usual), while displaying a façade of commitment.

Climate-friendly projects? The challenges of additionality and permanence

Several studies (see box below) have highlighted an overestimation of the climate gains achieved through carbon offset projects, due to a number of factors.

The construction of the reference scenario in determining the gains from carbon offsetting is obviously central: if the project designers overestimate the emissions of the reference scenario, this necessarily leads to the emission of too many carbon credits. This is a key issue, particularly in projects to combat deforestation or forest degradation (REDD+), where establishing a reference scenario is particularly complex. In an article published in 2020 44that 11 of the 12 REDD+ projects in the Brazilian Amazon had considerably overestimated the level of deforestation in the reference scenario, thus artificially inflating the level of emissions avoided by the projects and hence the associated carbon credits.

The additionality criterion for carbon offset projects is also a major factor in their effectiveness. A project is said to be additional when two conditions are met: firstly, the emissions avoided or sequestered would not have occurred without the project (reference scenario); and secondly, the project would not have come into being without the financial contribution made possible by carbon finance.

The real climate impact of a project also depends on its permanence.

Projects must not only demonstrate that emissions have been reduced or avoided (or that carbon has been removed from the atmosphere) in the immediate term, but also that the reductions achieved are permanent once the project has been completed. The definition of permanence is, of course, open to interpretation. Logically, it should be understood as the time required to keep carbon out of the atmosphere until humanity has succeeded in halting climate disruption and coping with its associated impacts. The Regulation establishing a Union certification framework for carbon removals, due to be adopted at the end of 2024, thus considers permanence to extend over a period of at least several centuries.

However, this criterion is not always respected, particularly in projects involving ecosystems, whether the aim is to avoid emissions by combating deforestation or to remove carbon from the atmosphere by reforesting(see section 3.2). For example, while Nespresso claimed to “offset” 95% of its capsule production by planting trees generating Verra-certified carbon credits, an investigation by Cash Investigation 37 revealed an overestimation of the climate gains announced, linked to a lack of project follow-up, with some trees having been cut down just a few years after being planted in Peru.

Some studies questioning the added value of offset projects for the climate

– According to a study by the Öko Institute published in 2016 46only 2% of projects covered by the Clean Development Mechanism(see section 4.1) have a high probability of guaranteeing environmental integrity criteria, i.e. ensuring that emissions reductions are additional and not overestimated.

– In 2024, in a literature review 47 of 14 studies covering 2,346 carbon reduction projects, representing around one-fifth of carbon credit emissions to date, the authors estimate that only 16% of credits issued constitute real reductions.

– At the request of Carbon Market Watch, the University of California at Berkeley studied the four main methodologies used by Verra 48the market leader, to certify REDD+ projects, which account for around a quarter of carbon credits issued to date. The findings are edifying: the 5 factors analyzed 49 all lead to too many credits being issued.

– According to a Greenpeace Canada report published in February 2024 50Shell sold 5.7 million “phantom credits” to oil sands producers over the period 2015-2021, for a total of CAD 200 million (€136 million). The oil company operates the Quest CO2 capture and storage plant in Alberta, Canada. The plant captures CO2 during bitumen processing operations in Canadian fields, then liquefies and injects it underground. In 2008, Shell obtained the right from the Alberta government to sell carbon credits representing 2 tCO2 for each tonne actually stored.

The various scandals relating to the climate efficiency of carbon offset projects, by highlighting the lack of monitoring of the quality and reliability of carbon credits, have encouraged a more demanding control dynamic.

So, in the summer of 2024, for the first time, Verra has just deleted some 40 projects from its register 51. These projects, involving rice farms in China that were supposed to reduce their methane emissions through better water management, were rejected for two reasons: lower-than-expected climate gains and lack of additionality, since these projects would likely have existed without the carbon market, with the Chinese government already encouraging farmers to turn to these water management practices.

The development of project certification methodologies at international level with the implementation of the UN Credit Facility(see box in section 4.2) may also have an influence in terms of standardization and reliability of project certification methodologies.

However, improved methodologies and rigor can only go so far.

The three criteria reviewed above clearly demonstrate the degree of uncertainty involved in quantifying a project’s climate impact. Taking this uncertainty into account in the methodologies would lead to a much smaller number of credits being issued than is currently the case, which would significantly increase the price of carbon credits. Would buyers be willing to pay for this? Particularly in view of the fact that communication on offsetting will become increasingly regulated.

More fundamentally, the question of permanence highlights the problem of the overall logic of offsetting. Almost half of all carbon credits issued to date are based on ecosystem management (whether through avoided deforestation, reforestation, afforestation, or carbon-storing agricultural practices): no matter how good the projects concerned, no developer can guarantee that the carbon will remain well-stored for centuries. Yet these projects are used to offset GHG emissions that we know will remain in the atmosphere for centuries.

As recommended by Carbon Market Watch,

There needs to be a fundamental shift away from the logic of offsetting. Companies and other users of carbon credits must clearly separate reporting on their contributions to forest conservation efforts from their own emission reduction efforts, rather than combining them into a single “net” figure that masks the true extent of their decarbonization.

Carbone 4 consulting firm 16which developed the NZI standard, recommends abandoning the term compensation and using the term contribution, which in no way implies that the tons of GHGs the company has helped to reduce, avoid or store are to be deducted from those it has emitted, either directly or indirectly. However, it remains important to publish these reduction efforts, which are necessary on a collective level, as we saw in the introduction.

Semantic bias, abdication of responsibility and inertia

The words “carbon credits”, “neutrality”, “neutralization”, “cancellation” and “compensation” operate a semantic bias that leads to the disempowerment of the players who use them.

The term offsetting implies that by purchasing a carbon credit, and thus contributing to the financing of a project outside its value chain, a company has the same impact on the climate as when it reduces its own emissions. However, this equivalence is inaccurate: the purchase of a carbon credit in no way cancels out the company’s emissions, which end up in the atmosphere and contribute to global warming.

There are very real economic reasons for this willingness to contribute to climate action by starting with others: buying carbon offsets today costs companies far less than projects to reduce their own emissions, which often require massive structural investment or even a rethink of their business model. On the other hand, as long as the company can announce that it has offset its emissions and become carbon-neutral, the benefits in terms of image and, where applicable, regulatory compliance, are equivalent.

Carbon offsetting thus fosters the illusion that climate change is a challenge that can be met with little effort, a few financial transactions and in isolation from other players in the economy. It does not encourage companies to rethink their business models to reduce their dependence on greenhouse gases. On the contrary, it pushes them into a kind of inertia that is harmful to the climate: if a company considers that it has “done the job” by buying carbon credits, who will take care of reducing emissions within its own perimeter?

Greenwashing, carbon offsetting and carbon neutrality

In the early 2020s, a number of cases highlighted the extent to which offsetting could lead to greenwashing, allowing many companies to proclaim themselves (or their products) as carbon neutral.

Here are just a few examples:

-In 2019, GUCCI, an Italian luxury brand, declared that it had achieved carbon neutrality after offsetting its emissions with REDD+ projects certified by Verra 53.

-In 2022, Air France offered its customers the option of “offsetting” the CO2 emissions associated with their journey 54.

– Until July 1, 2024, Green Choice, a Dutch energy company, was marketing “forest-compensated gas” to its customers. 55.

– Energy company Shell offers “carbon-neutral” lubricants on its website thanks to offsetting 56.

See also the report Carbon offsetting: anything but neutral! (2021) by CCFD-Terre Solidaire, which analyzes the carbon offset projects of 3 French and Swiss multinationals: Total, Air France and Nespresso.

In most cases, the companies concerned have been forced by scandal or greenwashing lawsuits to modify or even withdraw their communications on the subject. Public authorities are also increasingly taking up the issue. The EU updated its consumer protection legislation with the adoption of a directive in February 2024 57 which prohibits certain misleading claims, such as those asserting “that a product has a neutral, reduced or positive impact on the environment in terms of greenhouse gas emissions” on the basis of carbon offsetting.

For all these reasons, players promoting carbon neutrality standards are particularly attentive to the use and communication of offsetting by companies.

In the Net Zero Initiative reference framework, the purchase of carbon credits appears as a complementary action, to be distinguished imperatively from the efforts the company must make to transform its business model and make it compatible with the Paris Agreement. For the Science-based Target Initiative, the rule was to refuse to take carbon credits into account when building reduction trajectories for organizations. However, in April 2024, its Board sparked controversy by announcing, ahead of a revision of their flagship methodology, that carbon credits could now be substituted for corporate emissions reduction efforts. The controversy finally died down with the publication, in the summer, of two critical reports on offsetting 58 . This episode undoubtedly testifies to the pressure exerted by certain players in carbon finance, and even certain companies, to make offsetting appear as a fully-fledged decarbonization solution.

Conclusion

Achieving global carbon neutrality as quickly as possible is a gigantic challenge, and one that calls for strong and steady reductions in GHG emissions and the development of anthropogenic storage. The financial sums involved are considerable, and it is clear that governments will not be able to cover all of them. The private sector should therefore be called upon to contribute.

Carbon credits make this mobilization of private financing possible. But they should not be seen as “cancelling out” the GHG emissions of companies which, by purchasing these carbon credits, contribute to these reductions, avoidances or storages. This contribution can, however, be highlighted in their reporting.

Standards for calculating emissions or emissions trajectories must prohibit offsetting (this is currently the case for the two main standards, the GHG Protocol and SBTi). And voluntary markets must be abandoned in favor of regulated markets alone, which must be conducted with seriousness and professionalism.

- While the term carbon neutrality is not used as such in the Paris Agreement, the concept is defined in Article 4. ↩︎

- This aspect is developed in section 3.2. ↩︎

- To find out more about global warming, see the Economy, resources and pollution module. To understand the difference between greenhouse gas emissions and atmospheric concentration, see the sheet Counting greenhouse gas emissions. ↩︎

- Global average temperature is an indicator adopted by scientists and the international community to represent a certain level of climate change. Climate change manifests itself in many other ways than just rising temperatures (changes in precipitation patterns, an increase in the number and strength of extreme events, greater climate variability, rising sea levels, etc.). ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- CO2 is currently the only GHG that can be removed from the atmosphere. ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- The Global Carbon Project is a research program led by the international scientific network Future Earth. Every year, it publishes a benchmark report on the evolution of CO2 emissions worldwide, by country and by source (fossil fuels, land use change). It also includes the global carbon budget. ↩︎

- See the section on territorial emissions and carbon footprint in our Counting greenhouse gas emissions sheet. ↩︎

- It was instituted by law n°2015-992 of August 17, 2015 on energy transition for green growth. ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- Judgment no. 1904967-1904968-1904972-1904976 available on the Paris Administrative Court website. See also the Haut Conseil pour le Climat’s 2020 annual report: Redresser le cap, relancer la transition and the article Décryptage juridique de l’” Affaire du siècle “, Marta Torre-Schaub, The Conversation (10/02/2021). ↩︎

- The LULUCF sector refers to “land use, land-use change and forestry.” ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate. Emissions are made up of different greenhouse gases, but at present we only know how to remove CO2 from the atmosphere. The notion of tonnes of CO2 equivalent is therefore essential here, as it takes into account the “global warming potential” of the various gases. See our sheet on Counting GHG emissions. ↩︎

- Alain Grandjean, founder and chairman of The Other Economy, is also a founding partner of Carbone 4. Carbone 4 has no financial or editorial link with this page. ↩︎

- This is known as the carbon cycle, and refers to the circulation of carbon between the different compartments of our planet: the ocean, the biosphere (living beings), the atmosphere and the lithosphere (the earth’s crust, where carbon is stored in limestone and fossil fuels). ↩︎

- This situation is not without consequences: the increase in the oceanic carbon sink leads to ocean acidification, which is harmful to marine life (this is one of the planetary limits). Moreover, the situation may be reversed by the combined effect of human activities (which destroy terrestrial sinks) and global warming, which is harmful to old-growth forests (diseases, mega-fires, droughts, etc.). ↩︎

- Indeed, these flows will diminish in the future as the carbon cycle “stabilizes”. What’s more, these sinks are needed to offset some of the “on-board” warming caused by the inertia of the climate system. ↩︎

- According to the IPCC’s 2022 report, net emissions from the LULUCF sector are estimated at 6.1 GtCO2e/year over the 2010-2019 period, i.e. almost 10% of annual greenhouse gas emissions. Find out more about Carbon sinks: what are we talking about and what is their global potential, Carbone 4 2 (06/12/24) ↩︎

- Reforestation (or reforestation) consists in recreating forests in places where they have been destroyed in the past; afforestation (or afforestation) consists in planting trees to create forests on areas that have long (or even always, on the human timescale) been devoid of trees. ↩︎

- The former is known as DACCS(Direct Air Carbon Capture and Storage); the latter as BECCS(Bioenergy with Carbon Capture and Storage). ↩︎

- Howard Herzog, Jennifer Morris, Angelo Gurgel, Sergey Paltsev, Getting real about capturing carbon from the air One Earth, 2024. ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- See Puits de carbone: de quoi parle et quel potentiel au niveau planétaire, Carbone 4 noteCarbone4 (06/12/24) ↩︎

- Alain Grandjean, founder and chairman of The Other Economy, is also a founding partner of Carbone 4. Carbone 4 has no financial or editorial link with this page. ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- In 2024, the planet’s global temperature exceeded 1.5ºC above pre-industrial levels, but this does not mean that the objective of containing global warming below this threshold has been exceeded, due to short-term climate variations, in particular the El Niño phenomenon. See this excellent explanation by Christian de Perthuis on his blog: Le thermomètre au-dessus de 1,5°C en 2024 : quelles leçons en tirer? (10/01/2025). ↩︎

- Net Zero Initiative, A benchmark for collective carbon neutrality, Global objective on pillar C, 2020. ↩︎

- In 2024, the planet’s global temperature exceeded 1.5ºC above pre-industrial levels, but this does not mean that the objective of containing global warming below this threshold has been exceeded, due to short-term climate variations, in particular the El Niño phenomenon. See this excellent explanation by Christian de Perthuis on his blog: Le thermomètre au-dessus de 1,5°C en 2024 : quelles leçons en tirer? (10/01/2025). ↩︎

- Net Zero Initiative, Bâtir une stratégie de séquestration carbone à la hauteur des enjeux, 2023, p.13. ↩︎

- John H. Dales, Pollution, Property and Prices University of Toronto Press, 1968. He takes his inspiration from Ronald Coase, The problem of social cost, Journal of Law and Economics, 1960. ↩︎

- These are 38 developed countries plus the European Union. See the full list on the UNFCCC website. ↩︎

- These are 38 developed countries plus the European Union. See the full list on the UNFCCC website. ↩︎

- Called CERs – Certified Emission Reductions. ↩︎

- Nationally Determined Contributions (NDCs) were introduced by the Paris climate agreement (2015). These are national plans published by each state detailing their contribution to achieving the Paris targets. They include national GHG emission reduction targets, as well as public policies and measures to achieve them. The NDCs are non-binding and must be updated every 5 years. Find out more on theUNFCC website. ↩︎

- Emission Gap report 2024, United Nations Environment Programme. ↩︎

- Find out more about the difficulties of international negotiations on the implementation of Article 6:Resumption of climate negotiations: near-total lack of progress on key issues against a backdrop of deep divergences between Northern and Southern countries, Citepa, 2024;COP28: Article 6 failure avoids a worse outcome, Carbon market watch, 2023. ↩︎

- SeeTransitionof CDM activities to Article 6.4 mechanism, UNFCCC, consulted on 20/11/24. ↩︎

- The tonne of CO2 equivalent (Tonne eqCO2) is the unit used to aggregate the various GHGs according to their impact on the climate (find out more in our sheet Counting GHG emissions). ↩︎

- Philippe Delacote, Tara L’Horty, Andreas Kontoleon et al, Strong transparency required for carbon credit mechanisms, Nature Sustainability, 2024. ↩︎

- Voluntary Carbon Markets: Potential, Pitfalls, and the Path Forward, June 2024 ↩︎

- To find out more about the eight steps involved in creating a carbon credit, see Carbon Markets 101 – The ultimate guide to market-based climate mechanisms, Carbon Market Watch, 2024 (p.8). ↩︎

- Thales A. P. West et al, Overstated carbon emission reductions from voluntary REDD+ projects in the Brazilian Amazon. Proceedings of the National Academy of Sciences, 2020. ↩︎

- Superprofits: multinationals dress in green, Cash Investigation, first broadcast January 2023. ↩︎

- How additional is the Clean Development Mechanism? Öko-Institut, 2016. ↩︎

- Benedict S. Probst, Malte Toetzke, Andreas Kontoleon et al. Probst, Malte Toetzke, Andreas Kontoleon et al. Systematic assessment of the achieved emission reductions of carbon crediting projects, Nature Communications, 2024 ↩︎

- See Quality Assessment of REDD+ Carbon Credit Projects, Berkeley Carbon Trading Project, 2024, and Policy Brief Exposing the methodological failures of REDD+ forestry projects, Carbon Market Watch, 2024. ↩︎

- The factors are: the baseline scenario (what would have happened in the absence of the project); the risk of leakage (deforestation that moves to another location instead of being totally avoided by a project); forest carbon accounting (the amount of carbon stored in the forest protected by a project); project permanence (the risk of the protected forest being destroyed by man or natural causes at a later date); safeguards against negative impacts of the project on local communities or other environmental dimensions. ↩︎

- Selling Hot Air, Lessons from how Shell’s flagship carbon capture project sold $200M of credits for reductions that never happened, Greenpeace Canada, 2024. ↩︎

- For the first time, some 40 carbon credit projects written off for inefficiency, Novethic, 09/09/24 ↩︎

- Alain Grandjean, founder and chairman of The Other Economy, is also a founding partner of Carbone 4. Carbone 4 has no financial or editorial link with this page. ↩︎

- Gucci goes carbon neutral in attempt to tackle climate crisis, The Guardian, 12/09/2019. ↩︎

- Greenwashing: Air France reverses its carbon-offset option under pressure from associations, Novethic, 01/12/2024. ↩︎

- Aardgas met natuur voor morgen, Green Choice website (accessed 11/21/24). ↩︎

- See Delivering Carbon Neutral Solutions to Our Customers (accessed 11/21/24). In addition, the section of the site now called Shell environmental products, largely dedicated to offsetting, was called “Shell’s Carbon Neutral and Reduced Carbon Footprint Products” until 2023, according to the report Exposing the methodological failures of REDD+ forestry projects by Carbon Market Watch. ↩︎

- Directive no. 2024/825 of February 28, 2024, which must be transposed into national law by March 27, 2026. ↩︎

- To find out more, see SBTi: a way out of the carbon offset controversy? Carbone 4, 01/08/24. ↩︎